Why the cash collapse is not the story, the backlog is — and what investors are really being asked to underwrite.

TL;DR

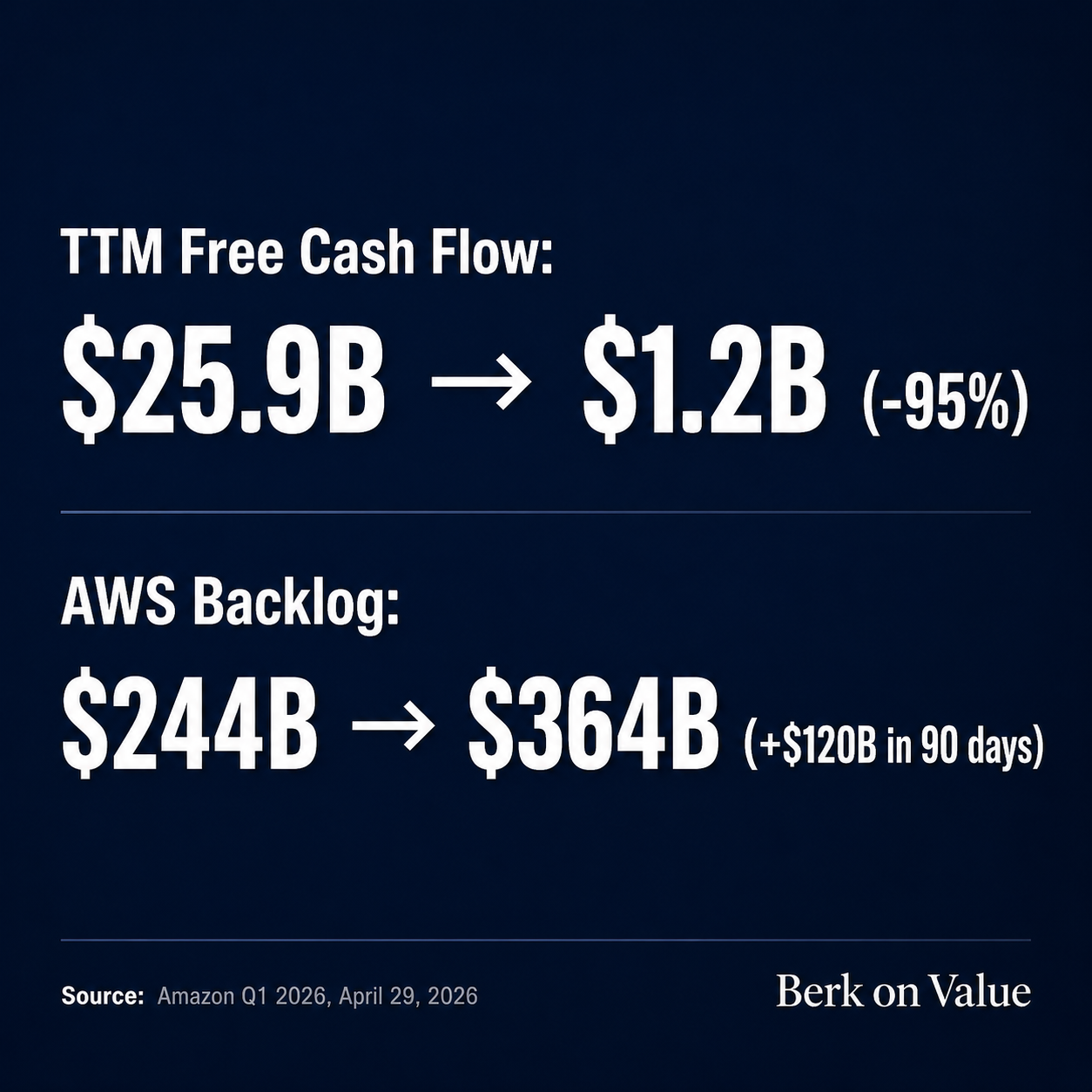

- Trailing twelve-month free cash flow fell 95% to $1.2 billion while Amazon spent $43.2 billion on capex in a single quarter.

- AWS revenue grew 28% to $37.6 billion — its fastest pace in more than three years.

- The AWS backlog jumped $120 billion in 90 days to reach $364 billion, and that figure excludes the new $100 billion-plus Anthropic deal.

- Amazon’s custom silicon program is now a $20 billion run-rate business with $225 billion in Trainium commitments.

- AWS added 3.8 gigawatts of power in twelve months — power has replaced chips as the binding constraint.

- The $11.57 billion Globalstar acquisition locks in direct-to-device satellite spectrum and extends Amazon’s stack into orbit.

- Retail funds the war: North America margins hit 9.0%, ads cleared $70 billion TTM, and Rufus is pacing toward $10 billion in incremental sales.

About this analysis

David Berkowitz manages the ValueAligned Portfolio at VAP Wealth Advisors and publishes Berk on Value, a free educational channel for long-term investors. His work focuses on quality compounders, capital allocation, and the gap between price and value across U.S. equities. New research is posted at vapwealthadvisors.com/berk-on-value-blog.

1. The “steady growth” Amazon is dead

For a decade, the Amazon story was retail discipline and slow margin expansion. Q1 2026 ended that story. Trailing twelve-month free cash flow collapsed from $25.9 billion to $1.2 billion — a 95% drop in a single year. Cash capital expenditures hit $43.2 billion in Q1 alone, and management has guided to roughly $200 billion in capex for the full year.

None of that stopped the operating numbers. Revenue grew 17% to $181.5 billion. Operating margin reached a record 13.1%. The cash isn’t gone. It has been redirected into the largest infrastructure buildout in the company’s history.

The hard truth: Amazon is asking the market to tolerate a near-zero cash floor for the next two to three years in exchange for owning the rails of the AI economy.

2. Amazon is now a top-three silicon player — and most investors missed it

The Trainium, Graviton, and Inferentia lines stopped being a side project. Viewed as a standalone business, Amazon’s chip operation now runs at a $20 billion annual rate, with nearly 40% sequential growth. At that trajectory, a $50 billion run rate is in reach, which would put Amazon third in the global data-center silicon market behind Nvidia and Broadcom.

CEO Andy Jassy disclosed over $225 billion in revenue commitments for Trainium. Trainium2 is sold out. Trainium3 — which started shipping at the start of 2026 — is 30 to 40% more price-performant than Trainium2 and nearly fully subscribed. Much of Trainium4, still 18 months from broad availability, is already reserved.

The big anchor tenants tell the story. OpenAI committed to roughly two gigawatts of Trainium capacity through AWS, ramping in 2027, and Anthropic is committed to up to five gigawatts of current and future Trainium generations. By owning the silicon, Amazon avoids the Nvidia tax and dictates the unit economics for everyone who rents from it.

Jassy on the call: “Customers are starving for better price performance.” That single line reframes the AI race from raw benchmarks to cost per token — and Amazon is the lowest-cost producer in the room.

3. The $364 billion backlog: most of the spend is already pre-sold

The headline figure from Q1 was not the capex. It was the contracted demand sitting behind it. The AWS backlog jumped to $364 billion, a $120 billion sequential increase in 90 days. That figure does not include the recently signed $100 billion-plus deal with Anthropic.

Add the two together, and roughly two-thirds of the $200 billion 2026 capex plan is already covered by signed contracts. Amazon also booked a $16.8 billion pre-tax gain on its Anthropic stake this quarter, separate from the cloud commitment.

There is one catch worth naming. Management has been explicit that there is a 6-to-24-month lag between assets going in the ground and revenue hitting the income statement. The cash leaves now. The revenue arrives in 2027 and 2028. The free cash flow collapse is a timing mismatch, not a demand problem.

When Morgan Stanley’s Brian Nowak asked about how concentrated the backlog was, Jassy said there is “reasonable breadth” beyond Anthropic and that AWS expects to sell Trainium racks externally as supply allows. The customer list is widening, not narrowing.

4. Power, not chips, is the new binding constraint

Two years ago the AI bottleneck was GPU supply. In 2026 the bottleneck is electricity. Management’s language on the Q1 call shifted noticeably toward gigawatts. AWS added more than 3.8 gigawatts of power in the last twelve months — more than any other cloud provider.

AWS has doubled its power capacity since 2022 and plans to double it again by the end of 2027. Wall Street estimates put AWS’s capacity at more than 31 gigawatts by year-end 2027, up from roughly 15 gigawatts in late 2025.

Read what that means: Amazon is becoming a utility infrastructure operator. The winners in AI will not be the ones with the cleverest models. They will be the ones who can secure substations, transmission rights, and water for cooling. Amazon got there first.

5. Retail and ads are quietly funding the war

The AI super-cycle dominates the headlines. The retail and advertising businesses are paying for it. Without that internal funding, Amazon would have to issue debt or dilute equity to keep up with hyperscale capex.

North America segment operating margin reached 9.0% in Q1, up from 8.0% a year ago, on $104.1 billion of segment revenue. The drivers are structural: direct-lane orders rose 40%, package touches dropped 20%, and miles traveled per package fell 19%. Same-day or overnight delivery hit one billion items in the quarter.

The ad business reached $17.2 billion in Q1 alone, putting trailing-12-month revenue over $70 billion. For context, that ad business is now bigger than all of AWS was in 2018.

AI is also showing up in the retail P&L. Rufus, Amazon’s generative shopping assistant, has reached 250 million users and is on pace to add $10 billion in incremental annualized sales. Customers who engage with Rufus are 60% more likely to complete a purchase.

6. The Globalstar surprise: Amazon is buying spectrum, not satellites

On April 14, 2026, Amazon announced an $11.57 billion all-cash acquisition of Globalstar — the second-largest deal in company history. The headline is satellites. The real asset is Globalstar’s globally harmonized Band 53/n53 spectrum, which is licensed across nearly every major market and effectively impossible to replicate today.

Combined with Amazon Leo (formerly Project Kuiper), which entered enterprise beta on April 8 ahead of a mid-2026 commercial launch, Amazon is moving toward a vertically integrated stack that runs from the data center to the device. The Apple iPhone satellite-connectivity agreement transfers with the deal, and Amazon plans to begin deploying its own direct-to-device system in 2028.

The strategic read: Amazon is no longer competing only with Microsoft and Google. It is also competing with Starlink and the carriers. The endgame is owning the connectivity layer that AI agents will run on.

What changed in Q1 2026 — at a glance

| Metric | Prior period | Q1 2026 |

| Revenue growth (YoY) | ~10–11% | 17% |

| AWS growth (YoY) | ~17% (early 2025) | 28% |

| TTM free cash flow | $25.9B | $1.2B |

| AWS backlog | $244B (Q4 2025) | $364B |

| Trainium revenue commitments | Not disclosed | $225B+ |

| North America operating margin | 8.0% | 9.0% |

| Advertising TTM revenue | ~$57B | $70B+ |

| Operating margin | ~11% | 13.1% (record) |

The real question for investors

Strip away the noise and the Q1 2026 print poses one question: at what point does a once-in-a-generation buildout justify a near-zero cash balance?

Amazon has answered that question with $200 billion. The 6-to-24 month yield lag means the $43.2 billion spent in Q1 will not show in revenue until 2027 or 2028. Investors are being asked to look past the cash collapse and trust three things at once: that the $364 billion backlog is real, that the gigawatts arrive on schedule, and that custom silicon margins hold up against Nvidia.

If those three trades land, Amazon owns the AI infrastructure layer for a decade. If any one of them misses, the cash drag becomes a credit story. The market’s reaction to the print — a wave of analyst price-target hikes after the call — suggests Wall Street has already taken the underwrite.

The only variable left is your time horizon.

This article is for educational purposes only and does not constitute investment advice. The ValueAligned Portfolio may hold positions in companies mentioned. Always conduct your own research or consult a registered investment advisor before making investment decisions.

Endnotes

- Free cash flow fell 95% to $1.2 billion — Seeking Alpha summary of Amazon Q1 2026 cash-flow impact from AI investment. https://seekingalpha.com/news/4581962-amazon-blows-past-aws-estimates-while-ai-investments-dent-free-cash-flow

- AWS revenue grew 28% to $37.6 billion — GeekWire coverage of AWS reacceleration in Q1 2026. https://www.geekwire.com/2026/aws-growth-climbs-to-28-as-amazons-big-ai-bets-start-to-pay-off/

- AWS backlog reached $364 billion (+$120B sequentially) — Amazon Q1 2026 earnings call transcript with Andy Jassy and CFO Brian Olsavsky. https://www.fool.com/earnings/call-transcripts/2026/04/29/amazon-amzn-q1-2026-earnings-call-transcript/

- Custom silicon hit a $20 billion run rate — The Register on Amazon’s chip business scale and growth. https://www.theregister.com/2026/04/29/amazon_chips_20b_business/

- AWS added 3.8 gigawatts of power in twelve months — Data Center Dynamics on AWS power capacity additions. https://www.datacenterdynamics.com/en/news/aws-added-38gw-of-data-center-capacity-in-the-last-year/

- $11.57 billion Globalstar acquisition — TechCrunch coverage of Amazon’s satellite-spectrum acquisition. https://techcrunch.com/2026/04/14/amazon-to-buy-globalstar-for-11-57b-in-bid-to-flesh-out-its-satellite-biz/

- Rufus on pace for $10 billion in incremental annualized sales — Fortune on Amazon’s AI shopping assistant monetization. https://fortune.com/2025/11/02/amazon-rufus-ai-shopping-assistant-chatbot-10-billion-sales-monetization/

- Free cash flow collapsed from $25.9B to $1.2B — TIKR analysis of Amazon Q1 2026 record operating margin and cash-flow drop. https://www.tikr.com/blog/amazon-posts-181-5b-revenue-and-highest-operating-margin-in-company-history

- Cash capex hit $43.2 billion in Q1 2026 — CNBC coverage of Amazon Q1 2026 earnings report. https://www.cnbc.com/2026/04/29/amazon-amzn-q1-earnings-report-2026.html

- Revenue grew 17% to $181.5 billion — Variety report on Amazon Q1 revenue beat. https://variety.com/2026/digital/news/amazon-earnings-q1-181-billion-1236733307/

- Record 13.1% operating margin — Bulios summary of Amazon Q1 2026 margin expansion. https://en.bulios.com/status/263435-amazon-q1-2026-revenue-grows-17-aws-accelerates-and-margins-continue-to-strengthen

- Andy Jassy on the rapid growth of Amazon’s chips business — About Amazon official Q1 2026 commentary on Trainium and silicon. https://www.aboutamazon.com/news/company-news/amazon-ceo-andy-jassy-amazon-chips-business-q1-2026-earnings

- Trainium3 is 30 to 40% more price-performant than Trainium2 — Converge Digest on Amazon Q1 2026 silicon performance. https://convergedigest.com/amazon-q1-2026-aws-surges-28-as-custom-ai-chips-top-20b-run-rate/

- OpenAI committed to roughly two gigawatts of Trainium capacity — About Amazon official Q1 2026 statement from Andy Jassy on AI customer commitments. https://www.aboutamazon.com/news/company-news/amazon-ceo-andy-jassy-aws-ai-q1-2026-earnings

- $16.8 billion pre-tax gain on Anthropic stake — Investing.com / GuruFocus highlights of Amazon Q1 2026 earnings call. https://ca.investing.com/news/company-news/amazoncom-inc-amzn-q1-2026-earnings-call-highlights-record-revenue-and-aws-growth-propel–4597835

- AWS doubled power since 2022 and plans to double again by 2027 — The Register on AWS $200B 2026 capex and power doubling plan. https://www.theregister.com/2026/02/06/amazon_earnings_q4_2025/

- North America operating margin reached 9.0% — HeyGoTrade Q1 2026 reaction on Amazon retail margin expansion. https://www.heygotrade.com/en/blog/amazon-q1-2026-earnings-reaction/

- Direct-lane orders +40%, package touches -20%, miles -19% — CityLogistics on Amazon Q1 2026 fulfillment efficiency. https://www.citylogistics.info/business/amazon-q1-2026-logistics-and-fulfillment-at-full-speed-but-at-what-cost/

- Advertising TTM revenue past $70 billion — Adweek on Amazon ad business scale. https://www.adweek.com/commerce/amazon-hits-70-billion-in-ad-revenue-over-the-past-12-months/

- Amazon Leo enterprise beta and mid-2026 commercial launch — TheNextWeb on Amazon Leo (formerly Project Kuiper) timeline. https://thenextweb.com/news/amazon-leo-satellite-internet-mid-2026

- Apple iPhone satellite-connectivity agreement — About Amazon official statement on Globalstar acquisition and Apple partnership. https://www.aboutamazon.com/news/company-news/amazon-globalstar-apple

- Globalstar Band 53/n53 spectrum — CNBC on Amazon’s $11.57B Globalstar acquisition and spectrum strategy. https://www.cnbc.com/2026/04/14/amazon-globalstar-satellite-leo-internet.html

- Wave of analyst price-target hikes after the print — 24/7 Wall St. on Wall Street reaction to Amazon Q1 2026 earnings. https://247wallst.com/investing/2026/04/30/wall-street-floods-amazon-with-price-target-hikes-after-q1-beat-is-aws-truly-the-ai-infrastructure-winner/