Ticker: MEDP | Event: Q1 2026 earnings release, April 22, 2026 | Stock reaction: ~20% drop

TL;DR

- Medpace posted Q1 2026 revenue of $706.6 million, up 26.5% year-over-year, yet the stock dropped roughly 20% after hours because forward indicators collapsed.

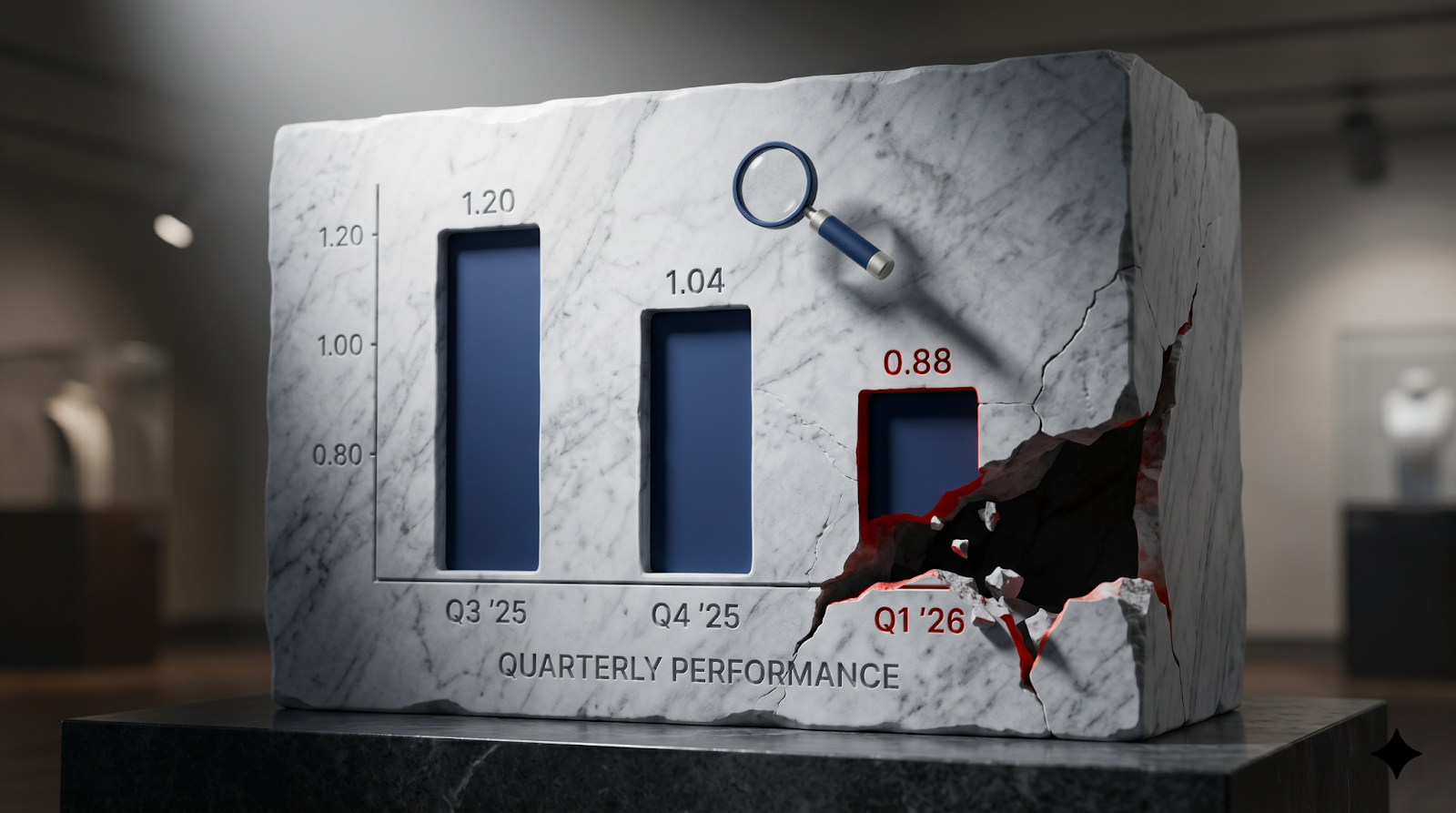

- The net book-to-bill ratio fell to 0.88, the weakest reading in more than a year and a steep drop from Q4 2025’s 1.04 and Q3 2025’s 1.20.

- CEO August Troendle told analysts the company has no sequential revenue growth for the rest of 2026, while management reaffirmed the $2.755B-$2.855B full-year guidance.

- Cancellations moved from the metabolic/GLP-1 bucket into oncology and cardiovascular, Medpace’s core therapeutic areas, breaking the firewall management built around the problem last quarter.

- President Jesse Geiger announced his retirement effective May 31, 2026 — he is a named individual defendant in the active securities fraud class action.

- Shareholders face a Levi & Korsinsky securities class action covering April 22, 2025 through February 9, 2026, with a June 8, 2026 lead plaintiff deadline.

About the author

David Berkowitz runs the ValueAligned Portfolio (VAP) model portfolio at VAP Wealth Advisors and publishes investing research under the Berk on Value brand (@BerkonValue on YouTube). He writes company-level research for long-term investors and produces educational content across YouTube, the VAP Wealth Advisors blog, LinkedIn, and Instagram. This analysis is for educational purposes only and is not investment advice.

The beat that wasn’t: what actually happened on April 22

Medpace posted Q1 2026 results on April 22, 2026. The headline numbers looked clean. The press release showed revenue of $706.6 million, a 26.5% year-over-year increase, and diluted EPS of $4.28 versus $3.67 in the prior-year period. Consensus EPS sat near $3.96, so the bottom line beat by roughly 8%. EBITDA grew 25.9% to $149.4 million. Operating cash flow landed at $151.8 million.

Then the stock collapsed. MEDP slid 20.8% after the print, with premarket trading on April 23 briefly marking shares near $380, erasing roughly $3 billion in market capitalization. The market was not pricing the quarter. It was pricing a set of forward admissions made during the Q&A.

A CRO trading near 30 times forward earnings is not paid for last quarter. That premium buys visibility into the next eight quarters. Remove the visibility and the multiple has no anchor. Three admissions from CEO August Troendle removed it.

- Gross new business awards were weak on their own merit, not just because of cancellations.

- Sequential revenue growth is absent for the remainder of 2026.

- Medpace must work on its win rate in a competitive market.

The book-to-bill collapse: 1.20 to 0.88 in two quarters

The single forward metric that matters for any contract research organization is the book-to-bill ratio: net new awards divided by revenue recognized. A ratio below 1.0 means the company is burning backlog faster than it is signing new work. A ratio of 0.88 means the sales motion is not keeping up.

| Quarter | Net New Awards | Net Book-to-Bill | Management Tone |

| Q3 2025 | $789.6M | 1.20x | “Well-behaved” |

| Q4 2025 | ~$737M | 1.04x | “Highest in over a year” |

| Q1 2026 | $618.4M | 0.88x | Spread across oncology, CV |

Baird analyst Eric Coldwell pressed Troendle on whether the 0.88 print was the result of unusual cancellations alone. Troendle answered directly: even if cancellations had landed at normal levels, book-to-bill still would have come in near 1.0. That answer ended the cancellation excuse. Gross new awards are the problem.

The chart is two quarters old at this point. Q3 2025’s record 1.20 book-to-bill drove shares to all-time highs. The Q4 2025 slip to 1.04 triggered the first sell-off in February. The Q1 2026 0.88 print is the third consecutive deceleration, not a one-off.

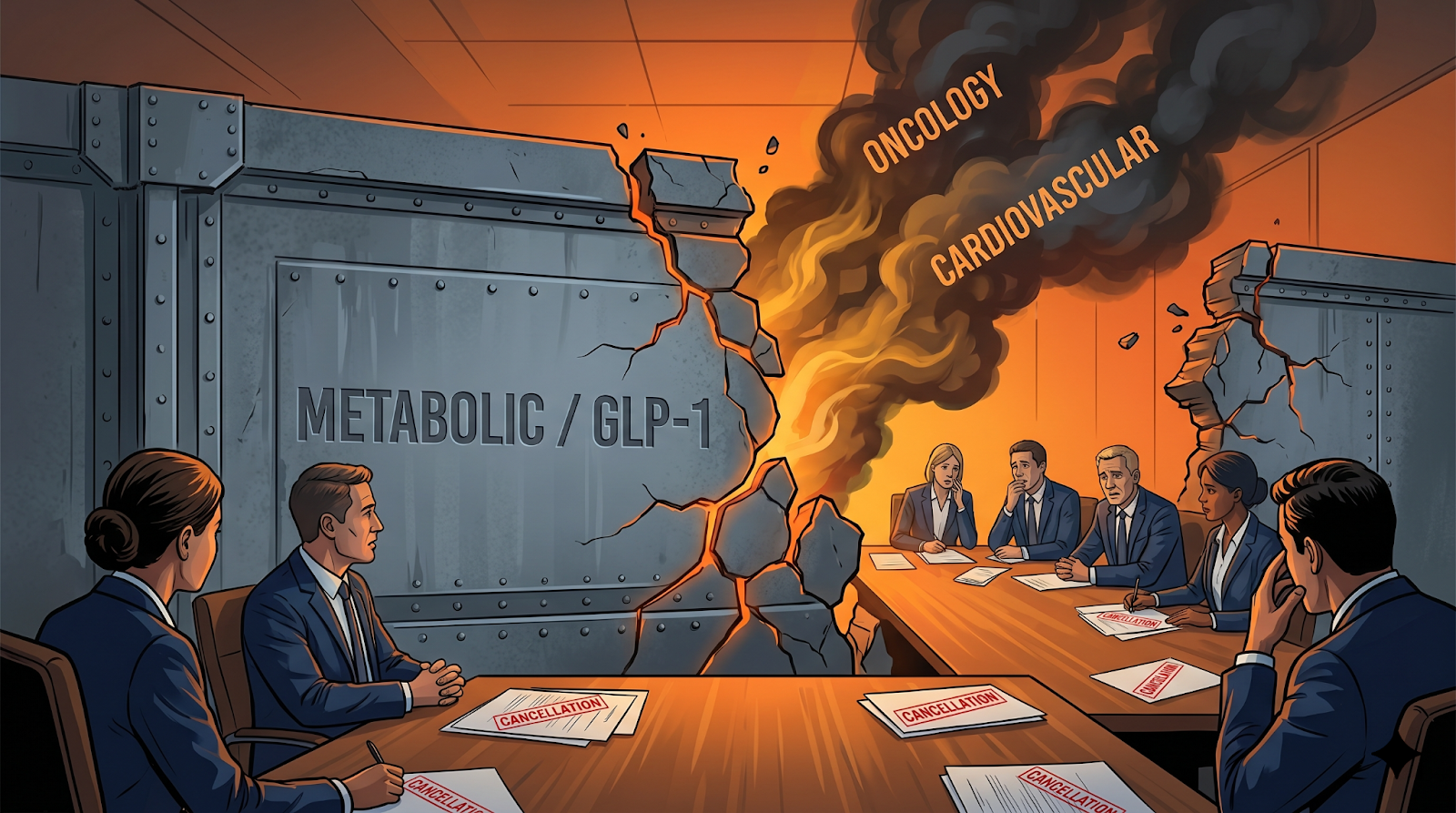

The firewall breach: cancellations now hit oncology and cardiovascular

Last quarter, management built a narrative firewall. On the Q4 2025 call, Troendle characterized cancellations as concentrated in the metabolic and GLP-1 bucket, framing the deterioration as narrow and transitory. Investors accepted that framing at the time.

The Q1 2026 call destroyed that defense. Troendle acknowledged the largest areas of lost business are now oncology and cardiovascular — Medpace’s historically strongest therapeutic areas. When analysts pressed for clarification, Troendle confirmed cardiovascular is a separate pipeline from metabolic. The cancellation problem is no longer contained.

This is a systemic clinical-funding headwind, not a sector-specific story. Biotech trial funding has tightened across therapeutic areas, and Medpace’s exposure to that funding cycle is now visible through its two largest revenue buckets.

The “elephant in the room”: six straight quarters of backlog decay

Institutional investors measure long-term revenue visibility using 12-month-plus forward backlog coverage — the portion of backlog scheduled to convert to revenue more than a year out. On the call, Baird’s Eric Coldwell flagged that this metric has declined for six consecutive quarters, a pattern he called “the undeniable elephant in the room.”

The Q1 2026 press release confirmed ending backlog of approximately $2.9 billion with $1.94 billion expected to convert to revenue over the next 12 months. The near-term conversion looks acceptable. The problem is what is not there: the second-year and third-year work that would normally sit behind the one-year bucket.

Troendle acknowledged the concern on the call, admitting earlier confidence was tied to rapid pre-backlog growth and an expectation cancellations would fall — “something that hasn’t happened.” Six quarters of the same direction is no longer a timing issue.

The guidance math: reaffirming $2.81B without sequential growth

The most damaging admission of the call concerned 2026’s shape. Troendle stated plainly: ” Looking at Q1 versus the remainder of the year, we do not have sequential revenue growth. We will on a year-over-year basis, but not sequentially.”

The CFO used the same call to reaffirm 2026 revenue guidance of $2.755 to $2.855 billion, a midpoint of $2.805 billion. Both statements cannot be equally true without a second-half bookings surge management cannot currently point to.

| 2026 Guidance Line Item | Range / Midpoint |

| Revenue | $2.755B – $2.855B (mid $2.805B) |

| EBITDA | $605M – $635M |

| GAAP Net Income | $487M – $511M |

| GAAP Diluted EPS | $16.68 – $17.50 |

| Share Repurchase Assumption | None — guidance excludes buybacks |

Adding to the pressure, Troendle conceded Medpace ” has to work on our win rate.” When Baird asked if the drop reflected intensifying competition, he answered: “I don’t know. How do you measure that? I just don’t have a way.” That is a rare admission from a CEO who typically defends Medpace’s sales execution. Hitting the reaffirmed number now relies on a recovery management that cannot currently be seen.

The executive exit: a named defendant retires mid-litigation

Buried inside the Q1 2026 release was a one-line disclosure: President Jesse Geiger notified Medpace of his intent to retire effective May 31, 2026 after 18.5 years with the company. The filing named no successor. CEO Troendle will reassume the President role on an interim basis.

The departure is not ordinary. Geiger is a named individual defendant in the active Levi & Korsinsky securities fraud class action, and the class period covers the very window in which he signed SEC filings and oversaw investor communications. A defendant executive retiring with no transition plan is the kind of single-sentence disclosure that drives institutional exposure reports the same week.

The litigation: a class period that matches the stock’s chart

Medpace is a defendant in a securities fraud class action filed by Levi & Korsinsky covering the period April 22, 2025 through February 9, 2026. Named individual defendants include CEO August Troendle, President Jesse Geiger, and CFO Kevin Brady.

The core allegation: management repeatedly guided to a projected 1.15 book-to-bill and described cancellations as “well-behaved” during the Q3 2025 call, when internal data allegedly showed elevated cancellations and deteriorating forward metrics. The lead plaintiff deadline is June 8, 2026.

The February 10, 2026 disclosure of the 1.04 Q4 book-to-bill drove MEDP shares down 15.9%, from $530.35 to $446.05. The April 22, 2026 Q1 print drove the next 20% leg down. The class-action chart aligns with the operating chart, which is what makes the legal overhang difficult to dismiss as opportunistic.

Multiple compression and the one remaining defense

Before the print, Medpace traded at roughly 29x trailing EV/EBITDA, nearly double IQVIA’s ~17x. The forward multiple compressed sharply as shares broke. A 30x multiple on a business delivering decelerating bookings, flat sequential growth, an executive exit, and an active class action is not defensible. The market is resetting Medpace toward the industry baseline.

Management’s one remaining defensive lever is capital return. Medpace ended 2025 with $821.7 million remaining on the share repurchase authorization and started 2026 with “a little bit over $800 million” available, per the Q1 call. The company did not repurchase shares in Q4 2025 or Q1 2026, preserving cash as the stock traded at premium valuations.

The current 2026 guide assumes no additional buybacks. That leaves an unused $800M lever sitting on a balance sheet with $652.7M of cash at March 31, 2026. At the compressed share price, an aggressive buyback becomes materially EPS-accretive and offers management a concrete way to set a floor under the stock. Whether the board uses it will tell investors more about conviction than any forward commentary.

What to watch: Q2 2026 is the binary resolving event

The bear thesis reduces to a single number. If Q2 2026 book-to-bill prints below 1.0, the reaffirmed guidance fractures and the April 22 sell-off becomes the first leg of a larger valuation reset. If the print recovers above 1.0 and shows the cancellation rate decelerating across oncology and cardiovascular, management’s “back-half recovery” narrative regains credibility.

Three data points to track between now and the Q2 2026 release

- Net book-to-bill trajectory, gross awards level, and the cancellation rate by therapeutic area.

- 12-month-plus forward backlog coverage — the six-quarter decline either breaks this quarter or it doesn’t.

- Whether Medpace executes any portion of the $800M+ buyback authorization in Q2 and whether a President successor is named before Geiger’s May 31 departure.

A 30x multiple is a bet on visibility. A 0.88 book-to-bill, sequential growth that disappeared, an executive exit, and an active class action together take that visibility off the table. The stock will trade on what replaces it.

Endnotes

- Q1 2026 revenue of $706.6 million, up 26.5% year-over-year — Medpace Q1 2026 press release mirror — PharmiWeb. https://www.pharmiweb.com/press-release/2026-04-22/medpace-holdings-inc-reports-first-quarter-2026-results

- Net book-to-bill fell to 0.88 — TradingView coverage citing Quartr transcript showing revenue up 26.5% with book-to-bill of 0.88. https://www.tradingview.com/news/urn:summary_document_transcript:quartr.com:3255410:0-medp-revenue-up-26-5-year-over-year-but-high-cancellations-pressured-book-to-bill-to-0-88/

- No sequential revenue growth for the rest of 2026 — GuruFocus recap of Q1 2026 earnings call highlights. https://www.gurufocus.com/news/8810882/medpace-medp-reports-strong-q1-2026-earnings-beating-expectations

- Cancellations in oncology and cardiovascular — Benzinga coverage of Q1 2026 rising cancellation disclosures. https://www.benzinga.com/markets/earnings/26/04/52012553/medpace-flags-rising-cancellations-near-term-growth-uncertain

- Jesse Geiger announced his retirement — Medpace Q1 2026 8-K disclosure via StockTitan — Geiger notified company April 21, 2026. https://www.stocktitan.net/news/MEDP/medpace-holdings-inc-reports-first-quarter-2026-taflbjtdbdp7.html

- Levi & Korsinsky securities class action — Levi & Korsinsky class action notice naming Troendle, Geiger, and Brady; class period April 22, 2025 – February 9, 2026. https://www.globenewswire.com/news-release/2026/04/20/3277437/3080/en/medp-investor-alert-medpace-holdings-inc-securities-fraud-lawsuit-investors-with-losses-may-seek-to-lead-the-class-action-after-ceo-allegedly-certified-misleading-statements-levi-k.html

- Diluted EPS of $4.28 versus $3.67 — Investing News Network coverage of Medpace Q1 2026 reported results. https://investingnews.com/medpace-holdings-inc-reports-first-quarter-2026-results/

- MEDP slid 20.8% after the print — Quiver Quantitative coverage on Medpace’s 20.8% slide tied to sub-1 book-to-bill and president retirement. https://www.quiverquant.com/news/Medpace+slides+20.8%25+as+Q1+book-to-bill+drops+below+1+and+president+retirement+is+disclosed

- Book-to-bill ratio: net new awards divided by revenue recognized — Pivotal Financial Consulting primer on CRO revenue metrics including book-to-bill. https://www.pivotalfinancialconsulting.com/single-post/2017/03/09/simple-metrics-clinical-research-organizations-should-utilize-but-dont

- Even if cancellations had landed at normal levels, book-to-bill still would have come in near 1.0 — StockStory deep dive on Medpace Q1 2026 call, Baird exchange. https://stockstory.org/us/stocks/nasdaq/medp/news/earnings-call/medp-q1-deep-dive-rising-cancellations-and-bookings-lag-shape-2026-outlook

- Q3 2025’s record 1.20 book-to-bill drove shares to all-time highs — Motley Fool transcript of Medpace Q3 2025 earnings call — Troendle “cancellations were well behaved” quote. https://www.fool.com/earnings/call-transcripts/2025/11/27/medpace-medp-q3-2025-earnings-call-transcript/

- Characterized cancellations as concentrated in the metabolic and GLP-1 bucket — Investing.com transcript of Medpace Q4 2025 earnings call. https://www.investing.com/news/transcripts/earnings-call-transcript-medpace-q4-2025-beats-expectations-stock-drops-93CH-4497135

- Baird’s Eric Coldwell flagged that this metric has declined for six consecutive quarters — Motley Fool transcript of Medpace Q1 2026 earnings call including Baird’s backlog-coverage question. https://www.fool.com/earnings/call-transcripts/2026/04/23/medpace-medp-q1-2026-earnings-transcript/

- Ending backlog of approximately $2.9 billion with $1.94 billion expected to convert — Seeking Alpha coverage of Medpace 12-month backlog conversion with cancellations rising. https://seekingalpha.com/news/4579135-medpace-sees-1_94b-backlog-conversion-over-next-12-months-as-cancellations-rise

- Looking at Q1 versus the remainder of the year, we do not have sequential revenue growth — GuruFocus earnings call highlights page for Medpace Q1 2026. https://www.gurufocus.com/news/8815325/medpace-holdings-inc-medp-q1-2026-earnings-call-highlights-strong-revenue-growth-amid-rising-cancellations

- Reaffirm 2026 revenue guidance of $2.755 to $2.855 billion — Medpace Q1 2026 press release mirror confirming reaffirmed 2026 guidance ranges. https://www.pharmiweb.com/press-release/2026-04-22/medpace-holdings-inc-reports-first-quarter-2026-results

- Has to work on our win rate — Investing.com Q1 2026 call transcript quoting CEO Troendle on win rate and competitive pressure. https://www.investing.com/news/transcripts/earnings-call-transcript-medpace-holdings-q1-2026-sees-earnings-beat-but-stock-tumbles-93CH-4633212

- Named individual defendant in the active Levi & Korsinsky securities fraud class action — Morningstar via Business Wire — Levi & Korsinsky notice on President Geiger allegations. https://www.morningstar.com/news/business-wire/20260421872030/medp-investor-alert-medpace-holdings-inc-securities-fraud-lawsuit-investors-with-losses-may-seek-to-lead-the-class-action-after-president-allegedly-oversaw-misleading-disclosures-levi-korsinsky

- Projected 1.15 book-to-bill and described cancellations as “well-behaved” — TipRanks summary of the class-action filing’s central allegations. https://www.tipranks.com/news/class-action/medpace-holdings-investors-face-lawsuit-over-alleged-misleading-guidance-on-key-business-metric

- MEDP shares down 15.9%, from $530.35 to $446.05 — Levi & Korsinsky alert citing Feb 10, 2026 price move tied to Q4 disclosure. https://www.prnewswire.com/news-releases/medp-investor-alert-medpace-holdings-inc-securities-fraud-lawsuit—investors-with-losses-may-seek-to-lead-the-class-action-after-company-allegedly-overstated-growth-projections-levi–korsinsky-302750016.html

- Medpace traded at roughly 29x trailing EV/EBITDA — AInvest CRO peer comparison placing MEDP near 29x versus IQVIA at ~17x. https://www.ainvest.com/news/cro-sector-quiet-revolution-medpace-iqvia-leading-charge-2507/

- Medpace ended 2025 with $821.7 million remaining on the share repurchase authorization — StockTitan 8-K coverage of Medpace 2025 results and buyback authorization balance. https://www.stocktitan.net/sec-filings/MEDP/8-k-medpace-holdings-inc-reports-material-event-a7a06ce7a613.html

- Assumes no additional buybacks — Investing News Network report on Medpace 2026 guidance assumptions. https://investingnews.com/medpace-holdings-inc-reports-first-quarter-2026-results/

- The largest areas of lost business are now oncology and cardiovascular — Benzinga coverage of rising cancellations in oncology and cardiovascular in Q1 2026. https://www.benzinga.com/markets/earnings/26/04/52012553/medpace-flags-rising-cancellations-near-term-growth-uncertain