How Q1 FY2026 turned Google from a search-ad cash machine into the world’s most capital-hungry AI infrastructure builder — and why the headline net income hides the real story.

By David Berkowitz · Berk on Value · Published April 30, 2026

TL;DR

- Alphabet reported Q1 FY2026 revenue of $109.9 billion, up 22% year-over-year — a $400 billion-base business that just accelerated, not slowed.

- Google Cloud crossed $20 billion in quarterly revenue (+63%) with a backlog that nearly doubled to $462 billion — enterprise AI is now the lead growth driver, not Search.

- Sundar Pichai told analysts Google is “compute-constrained in the near term” — demand exceeds supply, and Cloud revenue would have been higher with more capacity.

- Capex guidance was raised to $180–$190 billion for FY2026, with FY2027 set to “significantly increase” — putting the three-year build above $500 billion.

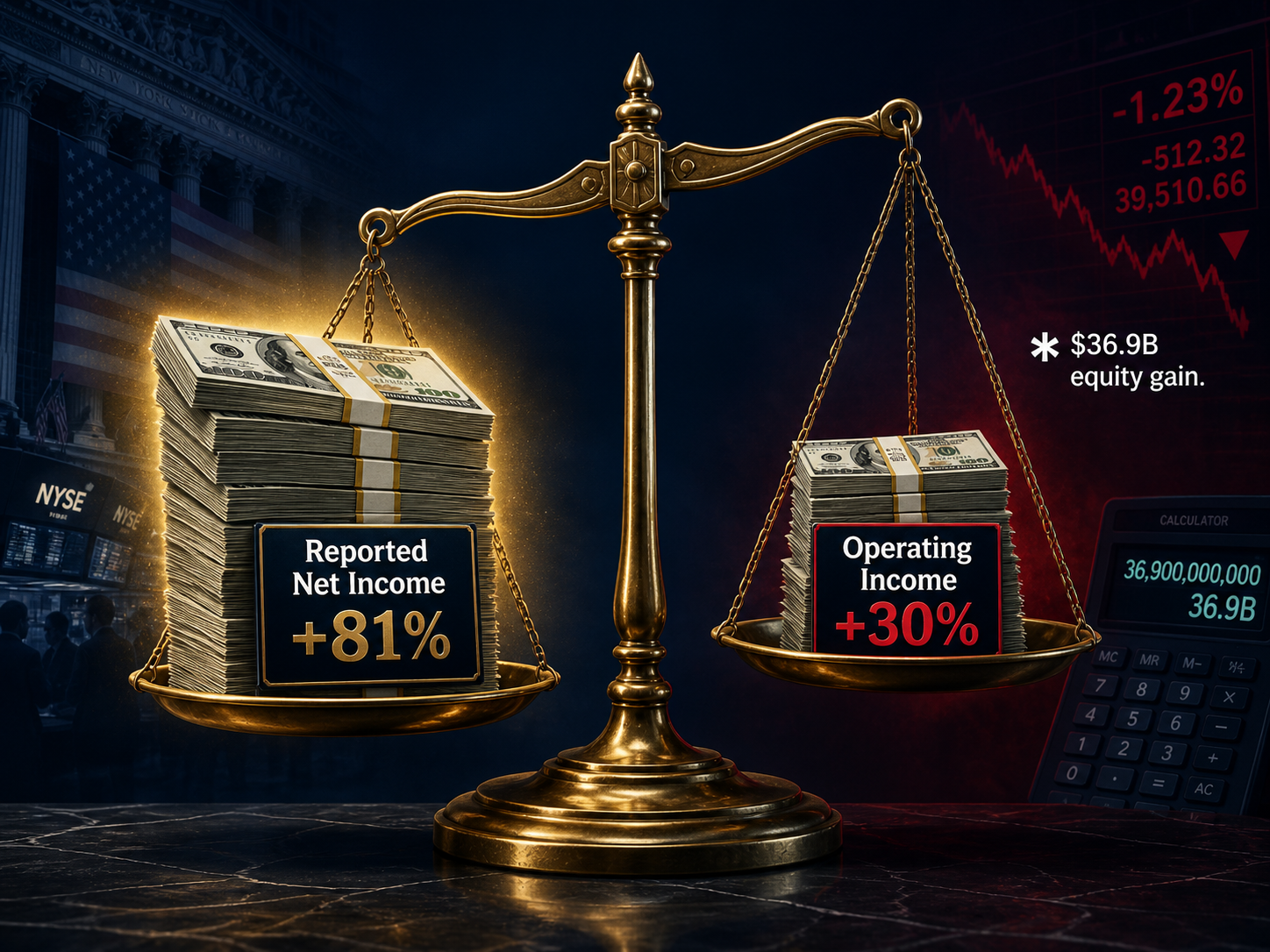

- The headline +81% net income looks heroic. Strip out the $36.9 billion non-cash equity gain and adjusted EPS came in at $2.62 — a one-cent miss versus consensus.

About the Author

David Berkowitz manages the ValueAligned Portfolio (VAP) at VAP Wealth Advisors and publishes investing research as Berk on Value. The portfolio focuses on long-duration compounders trading at fair prices. David analyzes hyperscaler capital allocation, AI economics, and durable competitive moats for a mass-affluent and high-net-worth audience. The analysis below uses Alphabet’s SEC filings, the Q1 FY2026 earnings release, the management call transcript, and primary IR disclosures.

This article is for educational purposes and is not investment advice. Author position: long Alphabet (GOOGL).

The unseen transformation

For two decades Alphabet ran on a single engine: search auctions and YouTube pre-rolls. That engine still hums. But behind it, Google quietly rebuilt itself into a capital-intensive AI infrastructure firm. The math is the giveaway. A $400 billion-revenue company should be slowing down. This one accelerated — from 14% growth a year ago to 22% in the quarter just reported.

The cost of that acceleration is steep. Alphabet is cannibalizing its own free cash flow to pour concrete, buy chips, and lock down power contracts. Pichai called the company “compute-constrained in the near term” — a status that means the world wants more Google AI than Google can deliver.

Below: five truths the market keeps getting wrong about this pivot, plus one bonus signal from Waymo. Each section names what changed, what it costs, and what could go wrong.

Truth #1 — The “search is dead” call was wrong. AI made it grow faster.

When AI Overviews and AI Mode launched, the bear case was simple: direct AI answers would gut the ad slots that pay for everything. Click-through rates would crater. Ad revenue would follow.

The data killed that thesis. Search & other revenue accelerated to $54 billion (+19%) in Q1 FY2026, up from 12% growth four quarters earlier. The driver: AI Mode pulled in users instead of pushing them out. AI Mode reached roughly 75 million daily active users and triggered query expansion — longer questions, more sessions, deeper engagement.

Management has held a consistent line on monetization. SVP Philipp Schindler told analysts AI Overviews monetize “at approximately the same rate” as standard Search, undercutting fears of margin dilution from the format shift.

“AI Mode is now used by tens of millions of people every day, and it is driving query growth and search satisfaction.” — Sundar Pichai, Q1 FY2026 earnings call

The bear case is not dead, just postponed. Network ads (third-party publisher revenue) fell 4% in the quarter — the first concrete sign that AI is reshaping traffic flows away from the open web. The AdSense slice is smaller than Search, but it is the canary.

Truth #2 — Cloud is the lead engine now, with a backlog that just doubled

For most of its history, Google Cloud was a cost center pretending to be a business. That changed this quarter. Cloud revenue hit $20.0 billion (+63%), operating margin expanded to 32.9%, and enterprise AI was cited — for the first time — as the segment’s primary growth driver.

The forward look is more striking than the print. Remaining performance obligations — contracted future revenue — nearly doubled sequentially to $462 billion, up from roughly $240 billion at the end of Q4 2025. Multiple billion-dollar deals closed in the quarter.

The shift to TPU as a product

On the call, Pichai disclosed a structural change in how Google sells AI compute. The company will start shipping its proprietary Tensor Processing Units (TPUs) into select customers’ own data centers — not just renting them through GCP. The flagship reference: Anthropic signed a multi-gigawatt TPU deal with Google and Broadcom, scaling up to one million TPUs. That single contract validates a hardware-as-product channel that did not exist as a line item six months ago.

AI Infrastructure snapshot

| Metric | Q2 FY2025 | Q1 FY2026 |

| Cloud revenue | $13.6B | $20.0B (+63%) |

| Cloud operating margin | 17.8% | 32.9% |

| Backlog (RPO) | $106B | $462B |

| GenAI product revenue (YoY) | — | +800% |

A near-term offset: the $32 billion Wiz acquisition closed March 11 and will create a low-single-digit-point margin headwind in Cloud through the rest of FY2026 as the security platform integrates.

Truth #3 — The bottleneck is not money. It is power, sites, and silicon.

Most CEOs spend earnings calls bragging about efficiency. Pichai used this one to admit the company is leaving revenue on the table because it cannot build fast enough. The constraint is physical: chips, electricity, and data center sites.

“We are compute-constrained in the near term. Our cloud revenue would have been higher if we were able to meet the demand.” — Sundar Pichai, Q1 FY2026 earnings call

That is a rare admission from a hyperscaler. It also signals where the next two years of capex will go: more substations, more long-term power purchase agreements, and aggressive procurement of newer accelerators — NVIDIA Blackwell, custom TPU v7 designs, and Broadcom-co-developed silicon.

CFO Anat Ashkenazi reinforced the urgency by raising guidance and flagging that FY2027 capex will “significantly increase” over FY2026. Translation: the build does not crest in 2026.

Truth #4 — The $500 billion receipt

Alphabet started 2025 guiding to $75 billion in capex. Each subsequent quarter brought an upward revision. The current trajectory:

| Year | Capex (guided / reported) | Source |

| FY2024 actual | $52.5B | Annual report |

| FY2025 actual | ~$91–$93B | Q4 FY2025 release |

| FY2026 guidance | $180–$190B | Q1 FY2026 call |

| FY2027 guidance | “Significantly increase” vs. FY26 | Ashkenazi, Q1 call |

Stack three years of guidance and the cumulative AI infrastructure bill clears half a trillion dollars. Alphabet is competing for the same scarce inputs as Microsoft, Meta, and Amazon — Big Tech’s combined Q1 FY2026 capex topped $650 billion of forward commitment. The grid does not scale to meet that on its own.

The risk is straightforward: if AI demand normalizes before these assets fully depreciate, return on invested capital slips toward the cost of capital. That is the ROIC reckoning baked into the timing.

Truth #5 — The 81% net income headline is an accounting accident

Most readers will see the 81% jump in Q1 net income and assume the AI flywheel is already throwing off historic profit. It is not. Alphabet booked a $36.9 billion non-cash gain on non-marketable equity securities — a mark-to-market revision tied to the increased value of private holdings. Strip it out and adjusted EPS lands near $2.62, roughly a penny below consensus.

The cleaner number is operating income, up 30% with operating margin at 36.1%. That is the figure that compounds. The $37 billion gain might reverse next quarter.

There are two more disclosure gaps to flag. First, management has declined to provide a duration framework for the $462 billion Cloud backlog — making it hard to model when contracted revenue actually books. Second, the antitrust overhang in search and ad tech remains unresolved, and management continues to avoid scenario analysis on remedies.

Bonus signal — Waymo crossed 500,000 paid rides per week

While the infrastructure fight rages in data centers, Alphabet’s autonomous-driving Other Bet hit a commercial milestone. Waymo is now delivering more than 500,000 fully autonomous paid rides per week across roughly 10 U.S. cities — ten times the May 2024 run rate. Recent launches include Dallas, Houston, San Antonio, Orlando, and Miami.

Waymo is no longer a science project. It is a scaled service competing with Uber and Tesla’s yet-to-launch robotaxi network. The “Up Next” expansion list — over 20 cities, including London and Tokyo — turns the unit from optional curiosity into a real call option on global mobility.

What to watch next

- Cloud backlog conversion. Watch how much of the $462 billion books as revenue per quarter — a 6–8 quarter conversion would be aggressive; 12–18 quarters is more realistic.

- FY2027 capex anchor. The first hard FY2027 number from Ashkenazi will tell investors whether the build crests near $220B or runs higher.

- TPU sell-in deals. Each new customer-data-center TPU contract is a step toward NVIDIA-style hardware revenue, not just GCP rentals.

- Antitrust remedies. Search and ad-tech rulings could force structural changes that reshape the cash flow profile materially.

- Network ads trend. If AdSense keeps falling, AI is reshaping the open web. That’s a multi-year story, not a quarterly noise item.

Alphabet now has more customers than it can serve and is spending more than any company in history to fix that. The binary question is simple: does AI demand stay vertical long enough to justify the build, or is the company laying concrete for a peak that has already passed? Q1 FY2026 says demand is winning. The next four quarters say which side compounds.

Endnotes

- 1. Q1 FY2026 results press release — Alphabet 8-K (SEC EDGAR): https://www.sec.gov/Archives/edgar/data/1652044/000165204426000043/googexhibit991q12026.htm

- 2. Q1 FY2026 earnings release PDF — Alphabet Investor Relations: https://s206.q4cdn.com/479360582/files/doc_financials/2026/q1/2026q1-alphabet-earnings-release.pdf

- 3. Alphabet Q1 FY2026 earnings call transcript — The Motley Fool: https://www.fool.com/earnings/call-transcripts/2026/04/29/alphabet-googl-q1-2026-earnings-call-transcript/

- 4. Pichai’s Q1 FY2026 prepared remarks — The Keyword (Google blog): https://blog.google/company-news/inside-google/message-ceo/alphabet-earnings-q1-2026/

- 5. Alphabet ups 2026 capex to as much as $190 billion, expects FY2027 to “significantly increase” — CNBC: https://www.cnbc.com/2026/04/29/alphabet-googl-q1-2026-earnings.html

- 6. Google Cloud surpasses $20B but says growth was capacity-constrained — TechCrunch: https://techcrunch.com/2026/04/29/google-cloud-surpasses-20b-but-says-growth-was-capacity-constrained/

- 7. Q4 FY2025 earnings release — SEC EDGAR: https://www.sec.gov/Archives/edgar/data/1652044/000165204426000012/googexhibit991q42025.htm

- 8. Google AI Mode hits 75M daily users — Search Engine Journal SEO Pulse: https://www.searchenginejournal.com/seo-pulse-ai-mode-hits-75m-users-gemini-3-flash-launches/563725/

- 9. AI Overviews monetization commentary (Schindler) — Search Engine Land: https://searchengineland.com/google-hypes-ai-overviews-refuses-to-answer-ctr-question-454637

- 10. Google Network ad revenue falls 4% in Q1 FY2026 — PPC Land: https://ppc.land/alphabet-q1-2026-google-network-ad-revenue-falls-4-as-ai-reshapes-the-web/

- 11. Google Cloud begins selling TPUs to select customer data centers — Let’s Data Science: https://letsdatascience.com/news/google-cloud-begins-selling-tpus-to-select-customers-44e44f48

- 12. Anthropic expands use of Google Cloud and TPUs (multi-gigawatt deal) — Google Cloud Press Corner: https://www.googlecloudpresscorner.com/2026-04-06-Anthropic-Expands-Use-of-Google-Cloud-and-TPUs

- 13. Anthropic, Broadcom, and Google chip deal coverage — The Register: https://www.theregister.com/2026/04/07/broadcom_google_chip_deal_anthropic_customer/

- 14. Google completes $32B acquisition of Wiz — Google Cloud Press Corner: https://www.googlecloudpresscorner.com/2026-03-11-Google-Completes-Acquisition-of-Wiz

- 15. Microsoft, Meta, and Google AI capex coverage — Fortune: https://fortune.com/2026/04/29/microsoft-meta-google-ai-capex-spending-billions/

- 16. Big Tech Q1 FY2026 earnings: $650 billion in AI capex and compute constraints — The Next Web: https://thenextweb.com/news/alphabet-amazon-meta-q1-2026-earnings-ai-cloud

- 17. Alphabet exceeds $100B in Q1 — AdExchanger (adjusted EPS detail): https://www.adexchanger.com/marketers/alphabet-exceeds-100-billion-in-q1-and-its-profits-almost-doubled/

- 18. Alphabet Investor Relations homepage — IR: https://abc.xyz/investor/

- 19. Waymo skyrocketing ridership chart — TechCrunch: https://techcrunch.com/2026/03/27/waymo-skyrocketing-ridership-in-one-chart/

- 20. Waymo expansion is leaving Tesla in the dust (Up Next list) — InsideEVs: https://insideevs.com/news/788284/waymo-expansion-tesla-cities-2026/