- Operating EPS increased 24% to $5.21, beating analyst estimates of $4.80, with revenue reaching $497.5 million ( Kinsale Q3 2025 Press Release).

- Combined ratio of 74.9% and nine-month operating ROE of 25.4% demonstrate sustained underwriting excellence ( ).

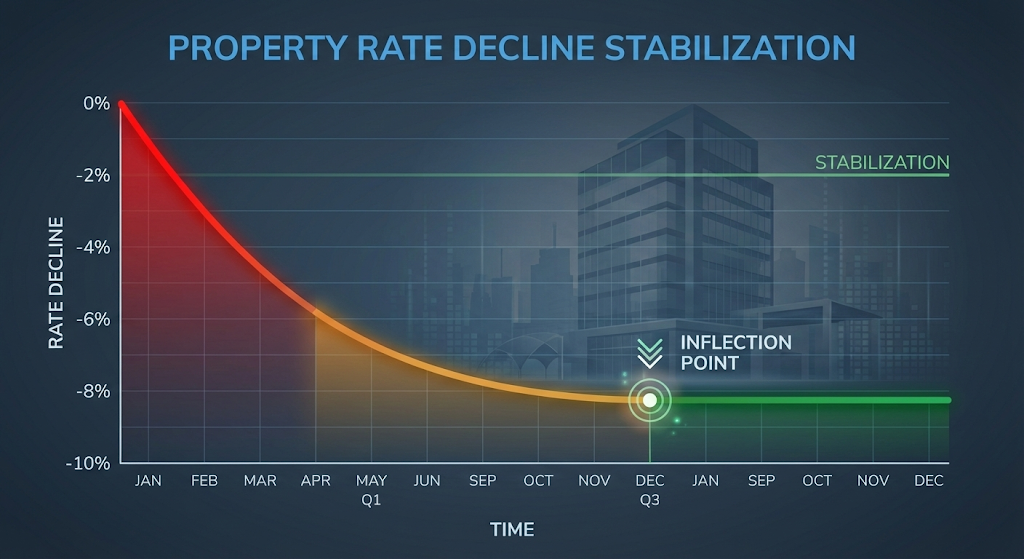

- Commercial Property rate declines stabilized from -17% in Q2 to -8% in Q3, signaling a market inflection point ( Yahoo Finance).

- Excluding Commercial Property, core growth was 12.3%, with double-digit expansion in Commercial Auto, Energy, and Agribusiness ( Fintool).

- Float grew 20% to $3 billion; book value per share increased 25.8% YTD ( Kinsale Q3 2025 Press Release).

David L. Berkowitz, Chief Investment Officer and Financial Advisor

Nearly 40 years of experience — from trading and research at a $250 million hedge fund in the early 1990s, to two decades as a portfolio manager, to teaching thousands of executives and employees how to create shareholder value through EVA and value-based management. Now helping individuals and families become shareholders through disciplined investing, concentrated portfolios, and direct stock ownership.

The narrative surrounding Kinsale Capital (KNSL) is caught in a growth paradox. To casual observers, the shift from 40%+ premium growth to 8.4% gross written premium growth in Q3 2025 looks like a cooling engine. This deceleration has sparked fears that the E&S specialist is losing ground in a crowded market.

The mechanics tell a different story. Kinsale is high-grading its portfolio while maintaining an elite 74.9% combined ratio and a 25.4% nine-month operating return on equity. The top line is normalizing. The bottom line reveals a company operating like a high-frequency trading firm that happens to write insurance policies.

1. The Property Inflection Point

What happened: Commercial Property premiums dropped 8% this quarter. The real story is the deceleration of decline. Rates fell 17% in Q2 but only 8% in Q3. President Brian Haney described a “positive second-order derivative” — the rate of decline is slowing ( Yahoo Finance).

Why it matters: The industry cannot sustain double-digit rate decreases indefinitely. This stabilization signals market rationalization. The E&S sector recorded an 88% combined ratio in 2024 versus 95% for the broader P&C industry, according to Fitch Ratings ( Fitch Ratings). Property lines recorded a 67% combined ratio versus 103% for casualty. Kinsale is positioned to re-engage selectively as rates find equilibrium.

2. The Technology Moat: Target State Architecture

What happened: Kinsale’s 21% expense ratio is not the result of belt-tightening. It is the output of their “Target State Architecture.” Two years ago, while competitors patched legacy systems from the 1980s, Kinsale began a ground-up rewrite of its entire enterprise system.

Why it matters: Kinsale’s proprietary technology platform offers an estimated 8-point advantage in expense ratio over peers, translating to a 5-point improvement in ROE ( Investing.com SWOT Analysis). Management views technology as a core competency on par with underwriting. Because they lack “thousands of legacy applications” plaguing traditional carriers, they integrate AI tools with implementation speed that competitors cannot match. This automation is deployed across three areas: IT development, underwriting submission processing, and claims resolution.

3. The Low-Cost Advantage in a Softening Market

What happened: A common misconception: Kinsale’s low-cost model is most valuable in a hard market. Reality: it is a more lethal weapon in a soft cycle. CEO Michael Kehoe noted an explosion of fronting companies — growing from one to approximately thirty in recent years — which often fund Managing General Agents (MGAs).

Why it matters: Business handled by MGAs reached $114 billion in premiums during 2024, with fronting carriers generating gross written premiums of $28 billion, up 26% over the prior year ( Gallagher Re/Risk & Insurance). These competitors frequently operate with expense ratios double Kinsale’s — often above 30% versus Kinsale’s 20-21% ( KoalaGains). As customers become intensely focused on cost, Kinsale offers competitive terms that still produce profit. This forces high-cost competitors into a lose-lose scenario: lose market share to Kinsale or operate at an underwriting loss.

4. Stealth Growth: Beyond the Headline Numbers

What happened: Strip away the volatile Commercial Property division and Kinsale’s growth was 12.3%. Net earned premium grew 17.8%, significantly outpacing the 8.4% GWP growth, driven by higher reinsurance retention ( Fintool).

Key growth segments include:

- Commercial Auto, Entertainment, Energy, Allied Health, Agribusiness, and Transportation — all posting double-digit growth

- Personal Lines — high-value homeowners remain a strategic emphasis

- New horizons — Ocean Marine and Aviation identified as expansion areas

Why it matters: This demonstrates management’s ability to reallocate capital toward niches that offer the best risk-adjusted returns rather than chasing volume in commoditized lines. CEO Michael Kehoe reiterated that 10-20% remains a “good conservative estimate” for growth potential over the full market cycle.

5. Financial Engineering and Capital Efficiency

What happened: The most striking figure: 17.8% growth in net earned premium versus 8.4% GWP growth. Higher reinsurance retention allowed Kinsale to keep more profit on its own books. Cash and invested assets totaled $4.9 billion at quarter-end, up from $4.1 billion at year-end 2024 ( ChartMill).

Why it matters: The $3 billion float, fueled by strong operating cash flows, drove a 25.1% increase in investment income. Management views the small dividend and share repurchase program as “dry powder” — latent capacity for shareholder returns as the company generates excess capital. Share repurchases of 45,627 shares at $20 million reflect disciplined capital allocation.

Q3 2025 Financial Snapshot

| Metric | Q3 2025 | Change vs Q3 2024 |

|---|---|---|

| Operating EPS | $5.21 | +24% |

| Revenue | $497.5M | +19% |

| GWP Growth | $486.3M | +8.4% |

| Combined Ratio | 74.9% | Elite |

| 9-Month Operating ROE | 25.4% | Industry-Leading |

| Book Value Growth (YTD) | $80.19/share | +25.8% |

| Float | $3.0B | +20% |

Leadership Continuity

Brian Haney, Co-founder and current President/COO, was elected to the Board of Directors. He will retire from his executive role in March 2026 to become a Senior Adviser focused on investor communications. This transition preserves the 30-year partnership between Haney and CEO Kehoe as a core asset. Stuart Winston was promoted to Executive Vice President and Chief Underwriting Officer. Management credited Winston’s team with delivering “some of the best underwriting results in the industry” ( Investing.com Transcript).

Key Quotes from Management

“Kinsale’s disciplined underwriting and low-cost business model is a consistent winner in an industry where the customers are intensely focused on cost.” — Michael Kehoe, CEO

“The fastest-growing participants in the market today are largely fronting companies, whose risk-bearing partners must contend with expense ratios often double ours or higher. And that math isn’t going to work out for them.” — Brian Haney, President & COO

“We’re hardwired to compete and win in this environment.” — Michael Kehoe, CEO

Conclusion: A Capital Efficiency Machine

Kinsale Capital is no longer a growth story. It is a capital efficiency story. With book value per share up 25.8% YTD and a business model that scales without a linear increase in costs, the firm has decoupled itself from the traditional insurance cycle.

The market may worry about single-digit top-line growth. The operational reality: Kinsale is a compounding machine. Traditional insurers, weighed down by legacy technology and bloated cost structures, are not competing with peers. They are competing against an engine designed to make their business models obsolete.

For investors: Watch for property rate stabilization translating into improved Commercial Property growth. Monitor the expense-ratio advantage as competitors work to close the technology gap. Track management’s capital allocation decisions as excess capital accumulates.

Endnotes

-

Kinsale Q3 2025 Press Release – Official Q3 2025 earnings announcement from Kinsale Capital Group Investor Relationshttps://ir.kinsalecapitalgroup.com/news/news-details/2025/Kinsale-Capital-Group-Reports-Third-Quarter-2025-Results/default.aspx

-

Yahoo Finance Q3 Deep Dive – Analysis of Kinsale Q3 2025 results and market dynamicshttps://finance.yahoo.com/news/knsl-q3-deep-dive-growth-201057685.html

-

Fintool Company Report – Comprehensive research report on Kinsale Capital Group financial performancehttps://fintool.com/app/research/companies/KNSL

-

Investing.com SWOT Analysis – Strategic analysis of Kinsale’s technology advantage and competitive positioninghttps://www.investing.com/news/swot-analysis/kinsale-capital-groups-swot-analysis-es-insurer-faces-growth-challenges-tech-edge-93CH-4277742

-

Gallagher Re/Risk & Insurance MGA Report – Analysis of MGA market growth and fronting carrier dynamicshttps://riskandinsurance.com/mga-market-surges-to-100-billion-as-fronting-carriers-spur-growth/

-

Conning MGA Study 2025 – Industry research on MGA premium trends and fronting company growthhttps://www.conning.com/about-us/news/ir-pr—mga-2025

-

Fitch Ratings E&S Report – Analysis of E&S market performance and combined ratioshttps://www.reinsurancene.ws/fitch-reports-seventh-year-of-double-digit-growth-for-us-es-insurance-in-2024/

-

AM Best E&S Market Report – WSIA-commissioned annual analysis of surplus lines market trendshttps://www.insurancejournal.com/news/national/2025/09/12/838828.htm

-

ChartMill Earnings Analysis – Q3 2025 earnings beat analysis and financial metricshttps://www.chartmill.com/news/KNSL/Chartmill-35832-Kinsale-Capital-Group-Inc-NYSEKNSL-Reports-Strong-Q3-2025-Earnings-Beat

-

Investing.com Earnings Transcript – Full Q3 2025 earnings call transcript with management commentaryhttps://www.investing.com/news/transcripts/earnings-call-transcript-kinsale-capital-q3-2025-earnings-beat-forecasts-stock-dips-93CH-4322148

-

KoalaGains Stock Analysis – Analysis of Kinsale’s expense ratio advantage versus industry peershttps://koalagains.com/stocks/NYSE/KNSL