A flexible, rules-based way to draw income in retirement — and why a fixed 4% is not the only option

TL;DR

- Guardrails set a starting retirement paycheck, then move it up or down on pre-agreed rules tied to how your portfolio performs — the approach Jonathan Guyton and William Klinger formalized in 2006.

- The idea is a response to — not a rejection of — Bengen’s 4% rule and the Trinity Study, both of which fixed spending in real terms regardless of market results.

- Because spending flexes, the original research found sufficiently stock-heavy portfolios could support starting withdrawal rates of 5.2% to 5.6% at a 99% confidence standard over 40 years.

- Morningstar’s recent work reached the same conclusion, giving guardrails the highest starting safe withdrawal rate of the systems it tested — near 5% versus roughly 3.7% for fixed real spending.

- The catch is real: adverse markets can force cuts. One 2024 Kitces analysis found Guyton-Klinger cutting real spending by 28% through the 2008 crisis and over 50% in a stagflation stress test.

- Done well, guardrails are a governance framework, not a spending trick — they work when the raise-and-cut rules are spelled out in dollars and wired into tax, Social Security, and RMD planning.

Who wrote this

David Berkowitz runs the ValueAligned Portfolio at VAP Wealth Advisors and publishes free educational investing content as Berk on Value. VAP Wealth Advisors is the trade name of ValueAligned Partners LLC, a Registered Investment Advisor. This piece translates the academic and practitioner research on retirement-income guardrails into plain language for people deciding how to draw a paycheck from a portfolio they spent a career building.

What a guardrails strategy actually is

Picture cruise control. You set a speed. The car eases off when the road tilts up and adds power when it tilts down, keeping you near the target without your foot on the pedal. Guardrails do the same for retirement spending. You set a starting paycheck, then two limits — one above, one below. Cross the top limit after a strong run, you get a raise. Cross the bottom limit after a rough stretch, you take a planned trim. Between the limits, nothing changes except an inflation bump.

This matters because the popular alternative is rigid. The 4% rule fixes your first-year withdrawal and then adjusts it for inflation every year after, no matter what the market does. That one-way ratchet is simple, but it ignores information. It keeps raising your spending into a bear market and keeps you underspending through a bull market. Guardrails use that information instead of throwing it away.

The trade at the center is worth stating flatly: you accept some year-to-year variability in your paycheck in exchange for a higher and more efficient paycheck over the full retirement.

Where the idea came from

The story starts with William Bengen’s 1994 paper. Using U.S. market history back to 1926, he found that a 4% first-year withdrawal, then adjusted for inflation, survived even the worst 30-year sequences. Four years later the Trinity Study reframed the question as portfolio success rates across withdrawal rates and stock/bond mixes, and found 3% and 4% rarely exhausted a diversified portfolio.

Jonathan Guyton asked the next question in 2004: is the safe rate too safe once you manage the withdrawals with rules rather than a fixed formula? Testing the brutal 1973 to 2003 stretch — two bear markets and a decade of high inflation — he found decision rules could push the safe starting rate to 5.8% to 6.2%, depending on stock allocation. In 2006, Guyton teamed with William Klinger and ran the rules through Monte Carlo simulation across thousands of paths. That paper added the two rules now synonymous with the term “guardrails” and concluded that portfolios with at least 65% stocks could sustain 5.2% to 5.6% starting withdrawals at a 99% confidence level over 40 years.

The four rules that run the system

Guardrails are usually described as two rules, but the full framework has four. Two govern spending. Two govern the portfolio behind it.

1. The withdrawal rule

Your paycheck rises with inflation each year, with one exception: after a year when the portfolio’s total return was negative and your current withdrawal rate is already above where you started, you hold the dollar amount flat instead of adding the inflation increase. No make-up later. The skipped raise is gone. Freezing one increase after a down year stops you from compounding the damage at the worst possible time.

2. The portfolio management rule

This decides which dollars fund the paycheck. After an asset class gains and drifts above its target weight, you sell the excess into cash to fund upcoming withdrawals. Then you spend in a set order: cash first, then bonds, then stocks — and you do not sell stocks to fund spending right after a down year if cash or bonds can cover it. You harvest winners and avoid forced sales of beaten-down stocks.

3. The capital preservation rule (the lower guardrail)

This is the brake. If a falling portfolio pushes your current withdrawal rate more than 20% above your starting rate, you cut the paycheck by 10%, and that lower number becomes the new base. The original research turns this rule off in the final 15 years of the plan, because late-retirement cuts sacrifice living standard without meaningfully improving the odds of the money lasting. This rule is the reason a higher starting paycheck is defensible — you have agreed in advance to pull back if the math demands it.

4. The prosperity rule (the upper guardrail)

This is the accelerator. If a rising portfolio pushes your current withdrawal rate more than 20% below your starting rate, you raise the paycheck by 10%, and that higher number becomes the new base. Without it, a cuts-only system would leave many retirees underspending through good markets and dying with money they could have enjoyed. Guyton and Klinger found the prosperity rule fires more often than the cut rule in many scenarios.

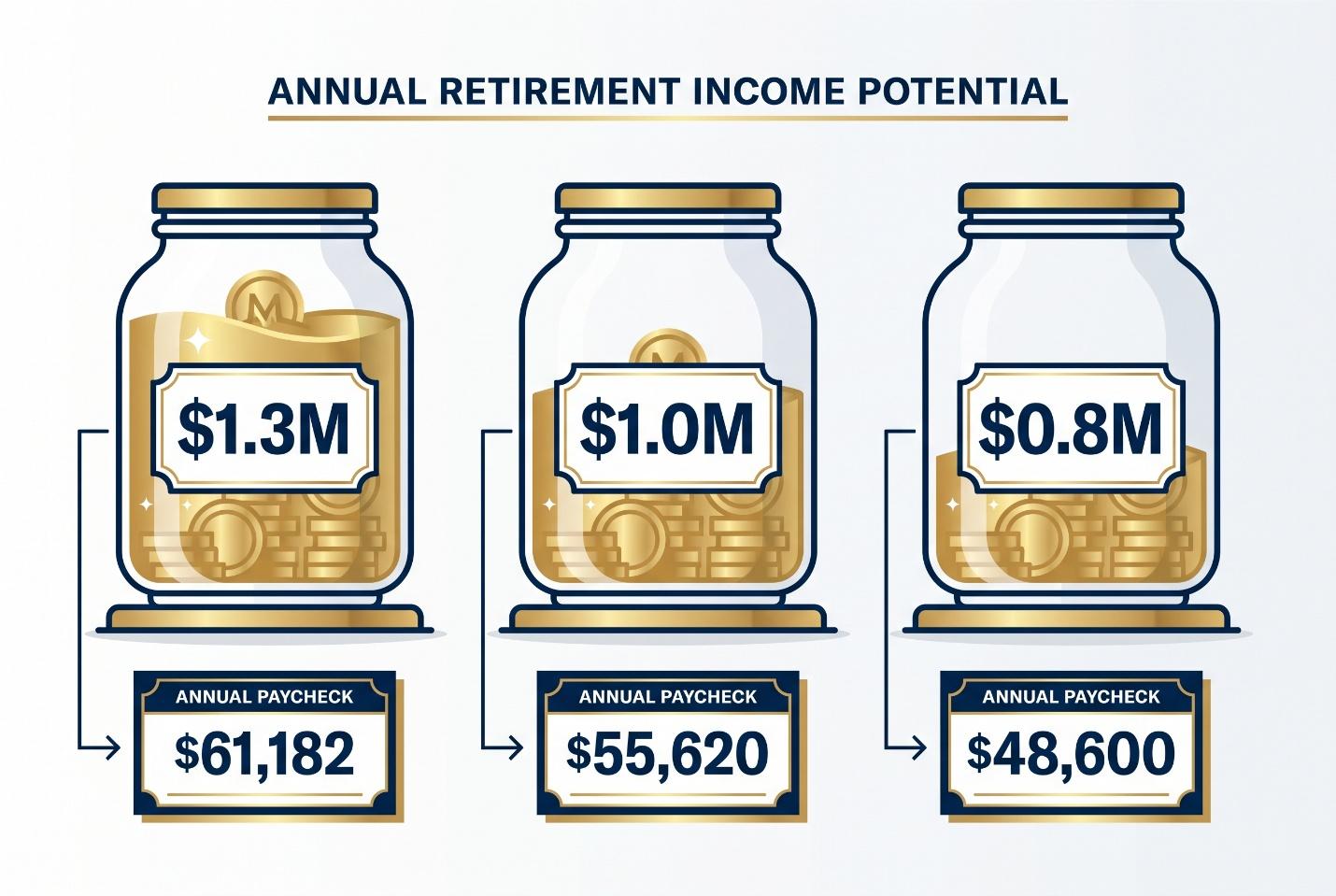

A worked example: $1,000,000 at 5.4%

Rules get abstract fast. Numbers do not. Say you retire with $1,000,000 and set a 5.4% starting rate — inside the range the 2006 research tied to high-confidence 40-year outcomes for a stock-heavy portfolio. Your first-year paycheck is $54,000. The 20% bands set your two triggers.

| Item | Calculation | Result |

| Starting portfolio | Given | $1,000,000 |

| Initial withdrawal rate | Given | 5.40% |

| First-year paycheck | $1,000,000 × 5.40% | $54,000 |

| Lower guardrail (cut) rate | 5.40% × 1.20 | 6.48% |

| Upper guardrail (raise) rate | 5.40% × 0.80 | 4.32% |

| Cut adjustment | $54,000 × 10% | −$5,400 |

| Raise adjustment | $54,000 × 10% | +$5,400 |

Now play three markets forward, one year on:

| Scenario | Portfolio value | Current rate | New paycheck |

| Prosperity (raise) | $1,300,000 | 4.28% – below 4.32% | $61,182 |

| No change | $1,000,000 | 5.56% – inside bands | $55,620 |

| Capital preservation (cut) | $800,000 | 6.75% – above 6.48% | $48,600 |

The strategy is client-friendly, not client-painless. You share in the upside when the portfolio outruns your spending. You also accept a real cut — here, from $54,000 to $48,600 — when losses push the withdrawal rate past the line. The advisor’s job is to decide, before that day comes, which dollars absorb the cut. Travel, gifting, a home project, and reinvested taxable income flex. The mortgage and the grocery bill do not.

How much more can guardrails support?

This is the payoff for accepting variability. Modern research keeps landing in the same place. In Morningstar’s testing, guardrails produced the highest starting safe withdrawal rate of any system studied — around 5% — against roughly 3.7% for fixed inflation-adjusted spending at the same 90% success target over 30 years. On a $1,000,000 portfolio, that gap is the difference between a $37,000 and a $50,000-plus first-year paycheck.

| Research | Style | Test | Core finding |

| Bengen 1994 | Fixed real | U.S. history since 1926 | 4% survived ~30-year horizons |

| Trinity 1998 | Fixed / inflation-adjusted | 1926–1995 | 3–4% rarely exhausted a diversified portfolio |

| Guyton 2004 | Decision rules | 1973–2003 stress | Safe start of 5.8–6.2% |

| Guyton-Klinger 2006 | Four rules | 40-year Monte Carlo | 5.2–5.6% at 99% confidence, 65%+ stocks |

Morningstar also found that Social Security stabilizes the ride. When a guaranteed check covers part of your spending, a portfolio cut hits a smaller share of your total income, so the swing you actually feel is gentler than the portfolio math alone suggests.

The honest tradeoff

A higher starting paycheck is not free, and any advisor who sells guardrails as a free lunch is doing it wrong. The cost is spending volatility, and in bad sequences it can bite hard. The sharpest critique comes from Derek Tharp and Justin Fitzpatrick at Kitces, who argue the original fixed-band version can overcorrect. Their stress tests put Guyton-Klinger real spending cuts at 28% through the 2008 crisis, 36% after the dot-com bust, and north of 50% in a stagflation scenario — far deeper than a plan that reads the full financial picture rather than a single withdrawal-rate band.

Two other costs are quieter. Complexity: you now have to understand inflation rules, band widths, adjustment sizes, and a spending order, not just one number. Discipline: the whole thing only works if you actually take the cut when the lower guardrail is breached. A guardrail you override is not a guardrail.

This is why the field has moved toward risk-based guardrails, which trigger on the health of your entire plan rather than a fixed withdrawal-rate line. For a household with a pension starting at 65, Social Security claimed at 70, and required distributions beginning at 73, a rigid 20% band can send false alarms during the bridge years. The core idea survives. The trigger gets smarter.

How we put guardrails to work

At VAP, guardrails are not a rule we hand you — they are a policy we write with you. Three things separate a plan that holds up from a spreadsheet that looks clever.

We speak in dollars, not percentages

Monte Carlo probabilities and withdrawal-rate bands mean nothing at the kitchen table. Kitces’ communication research makes the point plainly: clients need the numbers that move their life. So the plan reads like this — here is your paycheck, here is the portfolio value where it rises and by how much, here is the value where it falls and by how much. You know the raise and the cut before either happens, which is far calmer than watching a probability score drop and not knowing what comes next.

We map the cut before the market forces it

A 10% trim is tolerable when you decided in advance where it lands. We split spending into essential, important, and discretionary before setting a starting rate. For households with meaningful assets, we go further — separating lifestyle, gifting, charitable commitments, a second home, and opportunistic planning, because each has different flexibility and different meaning to you.

We wire it into tax, Social Security, and RMDs

The original portfolio rule is pre-tax and blind to account type. Real life is not. Which account funds each year’s paycheck — taxable, traditional IRA, Roth, or cash — changes your tax bill, your Medicare premiums, and your future required distributions. Required minimum distributions generally begin at age 73 for traditional accounts, while Roth IRAs carry no lifetime RMD for the owner — which makes Roth dollars valuable for late-retirement flexibility and legacy. When a cut is triggered, we can often soften the after-tax hit by changing which dollars fund spending before touching your lifestyle at all.

That is the real value of guardrails. Not a magic number. A written agreement about how your income responds to a future no one can predict — so that when markets get loud, the decision is already made, and calm.

If you want to see what a guardrails paycheck would look like on your own portfolio, that is a conversation worth having. Learn more about our work at VAP Wealth Advisors .

Endnotes

- Guyton and Klinger formalized guardrails in 2006 — Decision Rules and Maximum Initial Withdrawal Rates, Journal of Financial Planning — the paper that introduced the capital preservation and prosperity rules. https://www.financialplanningassociation.org/article/journal/MAR06-decision-rules-and-maximum-initial-withdrawal-rates

- Bengen’s 4% rule — William Bengen, Determining Withdrawal Rates Using Historical Data (1994) — archived overview of the original safe-withdrawal-rate study. https://robberger.com/research/determining-withdrawal-rates-using-historical-data/

- Trinity Study — Cooley, Hubbard, and Walz, Retirement Savings: Choosing a Withdrawal Rate That Is Sustainable, AAII Journal, February 1998. https://www.aaii.com/journal/199802/feature.pdf

- Guyton 2004 decision rules raised the safe rate to 5.8–6.2% — AssetBuilder summary of Jonathan Guyton’s 2004 decision-rules research. https://www.assetbuilder.com/knowledge-center/how-retirees-can-withdraw-more-than-4-percent-per-year

- Guardrails produced the highest starting safe withdrawal rate Morningstar tested — Morningstar, The Best Strategies for Boosting Starting Withdrawal Rates in Retirement. https://www.morningstar.com/retirement/best-strategies-boosting-starting-withdrawal-rates-retirement

- Social Security stabilizes the total-income experience — Morningstar, Finding Your Safe Withdrawal Rate — retirement-income research overview. https://www.morningstar.com/retirement/morningstars-retirement-income-research-finding-your-safe-withdrawal-rate

- Kitces: Guyton-Klinger can cut real spending 28% to over 50% — Derek Tharp and Justin Fitzpatrick, Why Guyton-Klinger Guardrails Are Too Risky For Retirees, Kitces.com (2024). https://www.kitces.com/blog/guyton-klinger-guardrails-retirement-income-rules-risk-based/

- Risk-based guardrails — Income Lab, Risk-Based vs. Guyton-Klinger Guardrails — comparison of trigger designs. https://incomelaboratory.com/risk-based-vs-guyton-klinger-guardrails/

- Communicate guardrails in dollars — Michael Kitces, Communicating Retirement Income Guardrails To Alleviate Monte Carlo Stress. https://www.kitces.com/blog/retirement-income-guardrails-monte-carlo-client-communication/

- Required minimum distributions generally begin at age 73 — IRS, Retirement Plan and IRA Required Minimum Distributions FAQs. https://www.irs.gov/retirement-plans/retirement-plan-and-ira-required-minimum-distributions-faqs

- Roth IRAs carry no lifetime RMD for the owner — IRS, Retirement Topics — Required Minimum Distributions (RMDs). https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-required-minimum-distributions-rmds

Disclosure

This article is for educational and entertainment purposes only. Nothing here is investment, tax, legal, or accounting advice. I am not your CPA, accountant, attorney, or tax professional, and I am not acting as your financial advisor in this article.

Investing involves risk, including loss of principal. Past performance does not predict future results. Markets, tax law, and individual circumstances change. Before acting on anything you read here, consult a qualified professional who knows your full situation.

Views expressed are my own and do not necessarily reflect the views of VAP Wealth Advisors.

Regulatory Information

ValueAligned Partners LLC is a Registered Investment Advisor. For additional information, please refer to our Form ADV, available on the SEC’s website at www.adviserinfo.sec.gov.