Dr. Ed Yardeni, who studied economics under Nobel Prize winner James Tobin at Yale and served at the Federal Reserve, projects the S&P 500 could reach 10,000 by 2030 in his “Roaring 2020s” scenario.

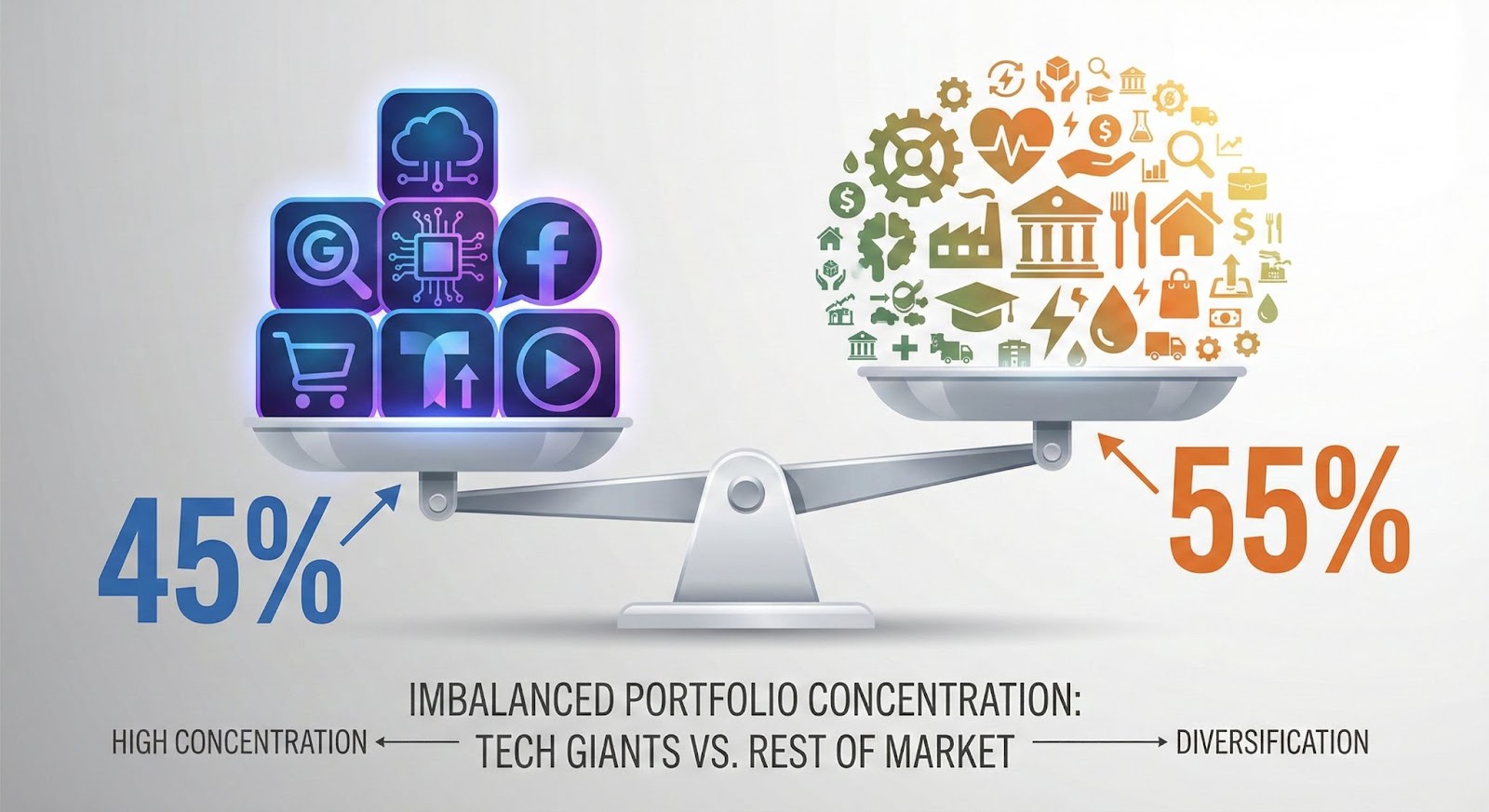

- Technology and Communication Services now make up about 45% of the S&P 500, a concentration level that Yardeni says warrants moving these sectors from “overweight” to “market weight” ( State Street).

- The “Magnificent 7” face new competition from AI challengers like DeepSeek while spending heavily on data centers—the Mag 7 invested nearly $265 billion in capital expenditures in their latest fiscal year ( GlobalData).

- Yardeni recommends shifting money to Financials (regional banks), Industrials (midcaps), and Healthcare (biotech), while adding international exposure as US stocks dominate global indexes at historically high levels ( Oppenheimer).

- Bond yields should stay between 4% and 5% despite Federal Reserve rate cuts—the 10-year Treasury currently sits around 4.22% ( Trading Economics).

David L. Berkowitz, Chief Investment Officer and Financial Advisor

Nearly 40 years of experience—from trading and research at a $250 million hedge fund in the early 1990s, to two decades as a portfolio manager, to teaching thousands of executives and employees how to create shareholder value through EVA and value-based management. Now helping individuals and families become shareholders through disciplined investing, concentrated portfolios, and direct stock ownership.

Who Is Ed Yardeni?

Before we dive into his market views, you should know who Ed Yardeni is and why his opinions carry weight on Wall Street.

Dr. Edward Yardeni earned his PhD in economics from Yale University in 1976, where he studied under Nobel Prize winner James Tobin ( Yardeni Research). He started his career at the Federal Reserve Bank of New York and held positions at both the Federal Reserve Board of Governors and the US Treasury Department. He later served as Chief Economist at major Wall Street firms, including EF Hutton, Prudential-Bache Securities, and Deutsche Bank.

Yardeni is also an accomplished author. His book Predicting the Markets shares insights from his four decades of forecasting economic trends. His second book, Fed Watching for Fun & Profit, helps investors understand how the Federal Reserve makes decisions—and how to profit from that knowledge.

In 2007, he founded Yardeni Research, Inc., which provides investment strategies to institutional investors worldwide. He appears regularly on CNBC and Bloomberg Television, and Barron’s magazine once dubbed him “Wall Street Seer” in a cover story ( Wikipedia).

What follows is a summary of Dr. Yardeni’s current market outlook. These are his ideas, not mine. I’m sharing them because his track record and credentials make his analysis worth understanding.

What Is the “Roaring 2020s” Thesis?

Yardeni believes we are living through a period similar to the 1920s—a time of rapid technological change that drives economic growth and stock market gains. Just as electricity and automobiles transformed the economy a century ago, today’s advances in artificial intelligence and digital technology are boosting productivity across every industry.

Think of “productivity” as getting more work done with the same effort. When companies become more productive, they can pay workers more, keep prices stable, and still make higher profits. Yardeni calls productivity “the fairy dust of the economy” because it makes everything work better at once ( Financial Sense).

Despite several crises—the pandemic, supply chain problems, inflation, and tariff battles—the US economy keeps hitting new records. Real GDP (the total value of goods and services adjusted for inflation) and consumer spending per household both sit at all-time highs. Yardeni sees this resilience as proof that the economy can handle whatever comes next.

His target: S&P 500 earnings reaching $500 per share by 2030, which would support an index level of 10,000—roughly 70% above current levels ( Benzinga).

Why Does Yardeni Say Big Tech Is Less Attractive for 2026?

The “Magnificent 7″—Apple, Microsoft, Alphabet (Google), Amazon, Meta (Facebook), Nvidia, and Tesla—have dominated stock market returns for years. But Yardeni sees a structural change underway.

These companies used to operate like separate kingdoms. Each dominated its own territory with little overlap. They generated enormous cash flows without spending huge sums to maintain their advantages.

AI has changed this dynamic. New competitors like DeepSeek (a Chinese low-cost AI provider) and Google’s Gemini can now challenge incumbents. The barriers that protected these giants are eroding, forcing them into an expensive arms race. The Magnificent 7 invested nearly $265 billion in capital expenditures in their latest fiscal year, up 27% from the prior period ( GlobalData).

Here’s why this matters for investors: when companies spend more on data centers, equipment, and talent, less money flows to profits and dividends. The Magnificent 7 profit growth is expected to slow to about 18% in 2026—down from much higher levels in recent years and only modestly better than the 13% growth expected from the other 493 companies in the S&P 500 ( Bloomberg via IndMoney).

For the first time since 2022, most of the Magnificent 7 underperformed the S&P 500 in 2025. Only Nvidia and Alphabet beat the broader market ( Yahoo Finance).

What Is “Market Concentration” and Why Does It Matter?

“Market concentration” refers to how much of the total stock market value sits in just a few companies. Right now, the Technology and Communication Services sectors account for about 45% of the S&P 500’s total market value. The top 10 holdings alone represent about 40% of the index ( State Street).

Picture a basketball team where one player takes 45% of all the shots. If that player has a bad game, the whole team suffers—even if everyone else performs well. The same logic applies to your portfolio. When nearly half your investment rides on tech stocks, any stumble in that sector hits your returns hard.

Yardeni recommends moving Technology and Communication Services from “overweight” (holding more than their index weight) to “market weight” (holding roughly their index weight). This doesn’t mean selling everything—it means reducing outsized bets on sectors that have already run up significantly.

Where Does Yardeni Suggest Looking Instead?

Yardeni points to the “Impressive 493″—the remaining companies in the S&P 500 that have been overshadowed by the Magnificent 7. He highlights three sectors as particularly attractive:

Financials, especially regional banks: Smaller banks often benefit when the economy grows steadily. They make money by lending to local businesses and homebuyers. When interest rates stay elevated (as Yardeni expects), banks earn more on their loans.

Industrials, particularly midcap companies: “Midcaps” are companies larger than small startups but smaller than giants like Boeing or Caterpillar. These businesses often provide equipment, machinery, and services that keep the economy running. They tend to perform well when economic growth is steady.

Healthcare, with a focus on biotech: Biotechnology companies develop new drugs and medical treatments. When larger pharmaceutical companies want new products, they often buy smaller biotech firms. This “M&A activity” (mergers and acquisitions) can reward biotech investors.

Yardeni’s 2026 Sector Allocation Strategy

| Sector | Previous Stance | 2026 Recommendation | Rationale |

|---|---|---|---|

| Tech / Comm Services | Overweight | Market Weight | 45% concentration; margin pressure from AI spending |

| Financials | Overweight | Overweight | Regional banks benefit from higher rates; attractive valuations |

| Industrials | Overweight | Overweight | Midcaps performing well; benefit from steady economic growth |

| Healthcare | Underweight | Overweight | Biotech M&A activity increasing; sector undervalued |

Should You Look Beyond US Stocks?

US stocks now dominate global indexes at historically high levels. International equities currently represent only about 27.5% of the MSCI World Index—their lowest weight in 40 years, compared to a long-term average of 48.7% ( Oppenheimer).

Yardeni suggests the “stay home” strategy that worked since 2010 may need revision. The US dollar has weakened by about 8-10% recently, boosting returns on foreign investments when converted back into dollars. International stocks also outperformed in 2025—the MSCI All Country World ex-USA index gained 29.2%, beating the S&P 500’s 16.4% return ( CNN).

He points to specific opportunities: Spain’s banking sector and Poland, Brazil, and Mexico as emerging-market plays. European defense spending has also created winners—German manufacturer Rheinmetall saw its share price rise 154% in 2025 as governments increased military budgets.

What About Bonds?

Many investors expected bond yields to fall sharply after the Federal Reserve started cutting interest rates. That hasn’t happened. Even though the Fed cut rates by 75 basis points in 2025 (and by 175 basis points total since September 2024), the 10-year Treasury yield has stubbornly stayed above 4%, currently around 4.22% ( Trading Economics).

Think of it this way: the Federal Reserve controls short-term rates, but the market sets long-term rates based on expectations for growth and inflation. Yardeni attributes the stubbornly high yields to “bond vigilantes”—investors who demand higher returns when they worry about government debt levels or persistent inflation.

Charles Schwab expects the Fed to cut rates two or three more times in 2026, bringing the target range to somewhere between 3.0% and 3.5% ( Charles Schwab). But long-term bonds may not follow suit. Yardeni expects the 10-year Treasury to trade between 4% and 5% for the foreseeable future.

Key takeaway: Don’t expect a return to the near-zero yield era. The economy is growing at a pace that supports higher bond yields.

How Does the S&P 500 Get to 10,000?

Yardeni’s path to 10,000 isn’t based on speculation or hoping for higher valuations. It’s an earnings story. Here’s his roadmap ( Financial Sense):

2025 S&P 500 earnings: approximately $268-$270 per share

2026 S&P 500 earnings: approximately $300-$310 per share

2030 S&P 500 earnings: approximately $500 per share

If the market applies a multiple of 20 times earnings (within his 18-22x range), $500 in earnings gets you to 10,000. That’s roughly 44% above today’s levels, spread across five years—an annualized return of about 11%, which is close to the stock market’s long-term historical average.

Yardeni expects this to be an “earnings-led” bull market rather than a “valuation-led” one. In plain English: stocks will rise because companies make more money, not because investors pay ever-higher prices for the same earnings.

When asked for the best investment advice he ever received, Yardeni didn’t hesitate: “Stay long.” His only regret? Not putting everything into the Nasdaq decades ago and never looking at it ( Benzinga).

What Should You Do With This Information?

Yardeni’s analysis provides a framework, not a guarantee. Markets can surprise even the most experienced observers. But his core message is practical:

- Review your tech exposure. If Technology and Communication Services make up more than 45% of your portfolio, consider rebalancing.

- Look beyond the headlines. The Magnificent 7 get the attention, but 493 other S&P 500 companies may offer better opportunities in 2026.

- Consider geographic diversification. US stocks dominate at historically high levels. Some international exposure could reduce risk and capture growth elsewhere.

- Set realistic expectations for bonds. Yields are likely to stay elevated. That’s not necessarily bad—4%+ yields provide meaningful income—but don’t count on a bond rally.

- Stay invested. Yardeni views market corrections as buying opportunities within a structural bull market, not reasons to panic.

The economy keeps surprising pessimists. Dr. Yardeni’s “Roaring 2020s” thesis suggests the good times may continue—but the easy money from loading up on tech stocks is probably behind us. The next phase rewards those who look beyond the obvious winners.

Endnotes

1. Yardeni Research Bio – Official biography detailing Dr. Ed Yardeni’s credentials, career history, and Federal Reserve experience.

https://archive.yardeni.com/yardeni-bio/

2. Wikipedia – Ed Yardeni – Background information on Yardeni’s career, including his Yale education under James Tobin.

https://en.wikipedia.org/wiki/Ed_Yardeni

3. Benzinga – S&P 500 At 10,000 – Coverage of Yardeni’s “Roaring 2020s” thesis and S&P 500 target.

https://www.benzinga.com/markets/equities/25/12/49492778/sp-500-at-10000-by-2030-yardeni-still-bets-big-on-the-roaring-2020s

4. Benzinga – Roaring 2020s Analysis – Detailed analysis of Yardeni’s sector recommendations and earnings forecasts.

https://www.benzinga.com/analyst-stock-ratings/analyst-color/25/11/49044503/ed-yardeni-analysis-roaring-2020s-sp-500-forecasts-2030-us-economy

5. Financial Sense – Roaring 2020s S&P 10,000 – Interview coverage of Yardeni’s earnings-based pathway to S&P 10,000.

https://www.financialsense.com/blog/21399/how-roaring-2020s-could-send-sp-500-10000-ed-yardeni-explains

6. Financial Sense – Gold and S&P 10,000 – Yardeni’s parallel forecasts for gold and equities.

https://www.financialsense.com/blog/21507/ed-yardeni-roaring-2020s-are-gold-and-sp-headed-10000

7. GlobalData – Magnificent 7 Capital Spending – Analysis of Magnificent 7 R&D and capital expenditure trends.

https://www.globaldata.com/media/business-fundamentals/magnificent-7-ramp-up-rd-and-capex-as-ai-shift-drives-2-trillion-revenue-surge-reveals-globaldata/

8. State Street – S&P 500 Concentration – Data on technology sector weight and market concentration.

https://www.ssga.com/us/en/institutional/insights/mind-on-the-market-17-november-2025

9. IndMoney – Magnificent 7 Outlook – Analysis of Magnificent 7 profit growth expectations for 2026.

https://www.indmoney.com/blog/us-stocks/is-magnificent-7-outperformance-over-2026

10. Yahoo Finance – Magnificent 7 Underperformance – Bloomberg data on Magnificent 7 performance vs. S&P 500.

https://finance.yahoo.com/news/magnificent-7-stock-market-dominance-140007016.html

11. Oppenheimer – 2026 Market Outlook – International equity weight in MSCI World Index and diversification analysis.

https://www.oppenheimer.com/news-media/2026/insights/oam/2026-market-outlook

12. CNN – International Markets 2025 – Performance comparison of US vs. international equities.

https://www.cnn.com/2026/01/04/investing/global-stock-market-year-international

13. Trading Economics – US Treasury Yields – Current 10-year Treasury yield data.

https://tradingeconomics.com/united-states/government-bond-yield

14. Charles Schwab – Fixed Income Outlook – Federal Reserve rate cut expectations and bond market analysis.

https://www.schwab.com/learn/story/fixed-income-outlook