The Dow Crashed 870 Points on Tuesday. Here’s What Smart Money Did Next.

- The Dow dropped 870 points on January 20, 2026—its worst day since October—after Trump threatened 10% tariffs on eight NATO allies over Greenland ( CNBC).

- Gold surged past $5,000 per ounce for the first time, with silver crossing $100—a historic flight to safe-haven assets ( CBS News).

- Q3 2025 GDP was revised up to 4.4%, confirming a “no landing” economy in which growth stays high but rate cuts are delayed ( Bureau of Economic Analysis).

- The CME FedWatch Tool shows a 95%+ probability that the Fed will hold rates steady at its January 27-28 meeting ( CME Group).

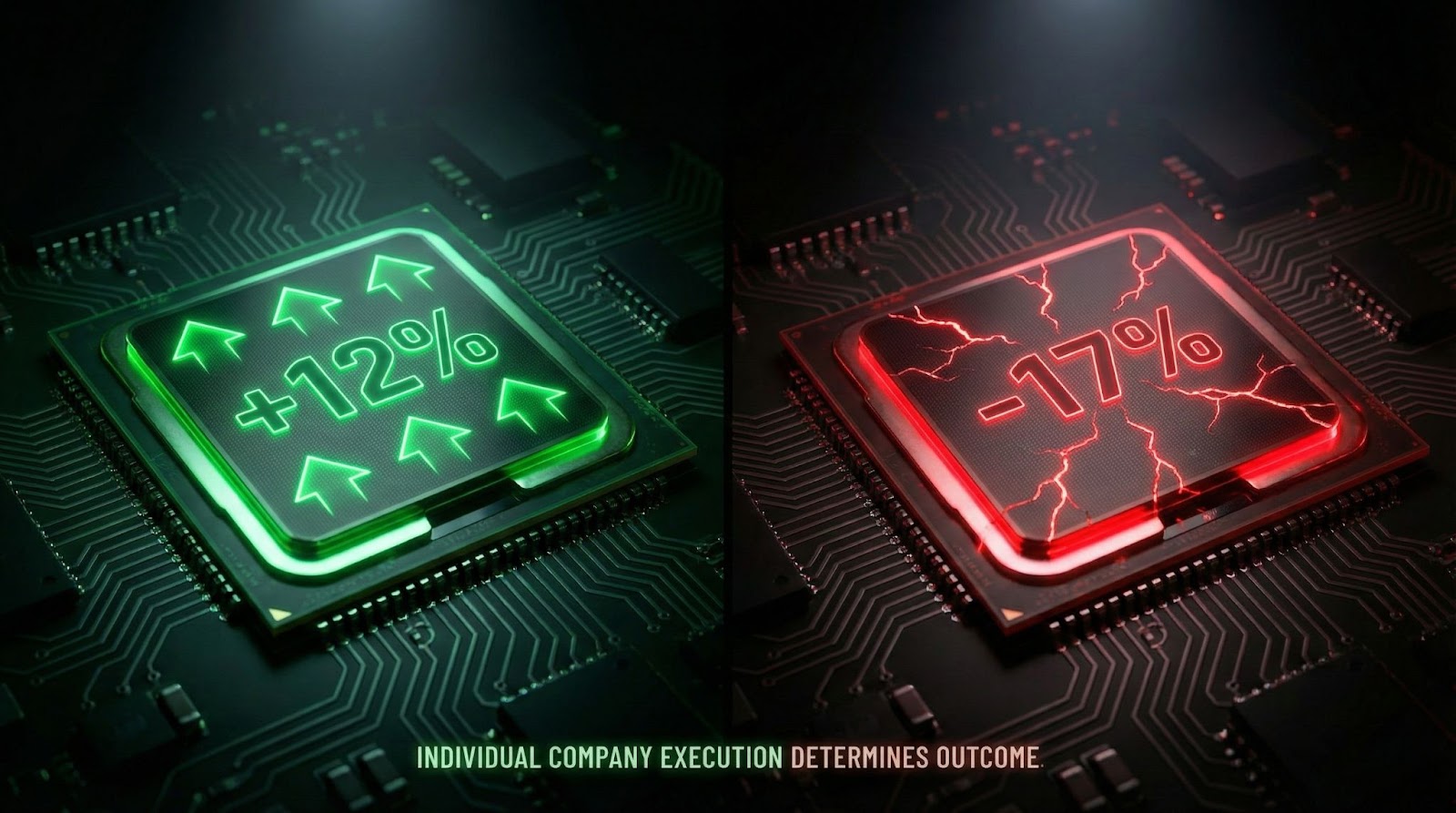

- AMD rose 12% while Intel dropped 17% in the same week—the semiconductor “stock selection” era has arrived ( Ad Hoc News).

What Triggered Tuesday’s 870-Point Crash?

The Greenland situation escalated fast. On Saturday, January 18, Trump announced via Truth Social that eight NATO members would face tariffs “until such time as a Deal is reached for the Complete and Total purchase of Greenland.” The targeted nations included Denmark, Germany, France, and the UK—major trading partners ( ABC News). Tariffs would start at 10% on February 1 and rise to 25% by June.

Tuesday delivered the market’s verdict. The Dow Jones Industrial Average shed 870.74 points, falling 1.76% to close at 48,488.59. The S&P 500 dropped 2.06% to 6,796.86. The Nasdaq Composite slid 2.39% ( Charles Schwab). The CBOE Volatility Index (VIX) spiked 10.3% to 20.78—its highest since November.

The “Sell America” trade triggered. Foreign investors fled U.S. assets. Treasury yields hit a four-month high. The dollar slid against major currencies ( Bloomberg).

Wednesday brought relief. A framework deal with NATO emerged. Tariff threats were withdrawn. Markets began recovering. By Friday, the S&P 500 had clawed back most losses, ending the week down just 0.35%.

But the damage to confidence persisted. Gold approached $5,000 per ounce—eventually breaking through on Sunday, January 26, to hit $5,104 ( Yahoo Finance). Silver crossed $100. These prices signal systemic distrust in policy stability now embedded in safe-haven assets.

Where Did the Money Move?

Sector performance shows exactly where capital fled during the crisis. Energy led with a 3.11% weekly gain. Oil prices rallied amid Middle East tensions and fears of tariff-driven inflation. When global uncertainty spikes, energy wins ( Charles Schwab Sector Outlook).

Materials followed closely. CF Industries, the fertilizer producer, gained 3.5%. Agricultural demand remains strong despite diplomatic noise.

The losers? Real Estate dropped 2.36%. High rates continue strangling valuations. Financials fell 2.5%, hurt by higher credit loss provisions. Capital One missed earnings badly.

The pattern: Defensive sectors and commodity producers outperformed. Rate-sensitive and trade-exposed sectors lagged. This rotation will continue as long as the Fed stays “higher for longer.”

Why Rate Cuts Keep Getting Delayed

The economy is accelerating when it was supposed to be cooling. Q3 2025 GDP was revised up to 4.4% from 4.3%—the strongest quarterly advance in two years ( Bureau of Economic Analysis). Growth was driven by consumer spending (+3.5%), exports, government spending, and investment.

But inflation remains stuck. The PCE price index increased 2.8% annualized in Q3, with core PCE (excluding food and energy) at 2.9% ( Barchart). Still above the Fed’s 2% target.

The labor market stays tight. Initial jobless claims totaled 200,000 for the week ending January 17—below the 209,000 consensus estimate and near the lowest levels in two years ( Department of Labor). Employers are hoarding workers despite tech layoffs making headlines.

This is the “No Landing” scenario. Growth stays high. Inflation stays elevated. Rate cuts get delayed. The market once expected five or six cuts in 2026. Now it prices fewer than two. The first cut might not come until July ( Morningstar).

For investors, this means favoring companies with pricing power and low debt. AutoZone. Ulta Beauty. Businesses that can pass costs to customers and don’t need cheap financing to grow.

What to Watch at the Fed Meeting

The Fed enters its blackout period ahead of the January 27-28 meeting. The CME FedWatch Tool shows a 95%+ probability they hold rates steady ( CME Group). The current federal funds target range sits at 3.50%-3.75% after three consecutive quarter-point cuts in late 2025.

One political risk demands attention. The DOJ launched an unprecedented criminal investigation into Fed Chair Powell over his Congressional testimony regarding headquarters renovations. Powell called the probe “political intimidation” and a direct assault on Fed independence ( Federal Reserve Statement). Markets hate uncertainty about central bank autonomy.

Powell’s term as Chair ends in May. Trump has said he already selected a replacement ( CNBC). His press conference on Wednesday will be critical. His language on the 4.4% GDP strength could trigger a “higher for longer” sell-off if he sounds hawkish.

Why Chip Stock Selection Now Matters More Than Sector Bets

AMD surged 12% for the week, up 21% year-to-date. The “anti-Intel” trade crystallized.

Intel beat Q4 earnings expectations with revenue of $13.7 billion and adjusted EPS of $0.15. But guidance destroyed the stock: Q1 2026 revenue projected at $11.7-$12.7 billion, below consensus. Adjusted EPS forecast at $0.00. The stock dropped 17% in a single day—its worst loss in 18 months ( Ad Hoc News).

CFO David Zinsner described Q1 as a “hand-to-mouth” quarter with depleted buffer inventory and acute supply constraints ( Stocktwits). AMD became the primary beneficiary. KeyBanc analyst John Vinh noted AMD is effectively sold out for 2026 on server processors, with potential to raise prices 10-15% in Q1.

The message for investors: The days of buying “semis” as a monolithic trade are over. AMD up 12%. Intel down 17%. Same sector. Opposite results. Stock selection within sectors matters more than sector selection itself.

Three Takeaways for Long-Term Owners

1. Geopolitics is tradeable risk now. The “Sell America” reaction was swift and severe—870 points in a single session. U.S. policy volatility is now a priced factor in global markets. Tuesday’s panic created buying opportunities for patient capital, not selling emergencies.

2. The “No Landing” economy cancels both recession fears and imminent rate cuts. With 4.4% GDP growth, the economy is neither overheating nor stalling. Favor companies with low debt and high pricing power. They don’t need cheap financing to grow.

3. Semiconductor selection is critical. The monolithic “buy semi stocks” trade is dead. Execution matters. AMD up 12%. Intel down 17%. Owning the wrong chip stock is now a liability, not just underperformance.

What to Watch Next Week

The week of January 26-30 is the most consequential of Q1. A convergence of macro and micro events will dictate market direction.

Wednesday, January 28: Fed decision and Powell press conference. Rate hold expected. The guidance language matters more than the decision.

Big Tech earnings: Roughly 20% of the S&P 500 reports. Microsoft, Apple, Alphabet, Tesla. Big Tech guidance will determine whether AI capital spending translates to actual revenue ( FactSet).

Economic data: Employment Cost Index and JOLTS job openings. Both give clues on wage inflation—key inputs for the Fed’s inflation model.

Bull case: Fed acknowledges falling inflation. Microsoft and Apple confirm AI spending is generating revenue. Nasdaq breaks resistance at 26,000.

Bear case: Powell sounds hawkish on the GDP data. Apple or Microsoft offer tepid guidance similar to Intel’s disaster. S&P 500 tests support at 6,800.

Endnotes

- CNBC Markets – Live updates on the January 20, 2026, market sell-off following Trump’s Greenland tariff threats.https://www.cnbc.com/2026/01/19/stock-market-today-live-updates.html

- CBS News – Gold breaks $5,000 per ounce for the first time amid geopolitical uncertainty.https://www.cbsnews.com/news/gold-breaks-5000-per-ounce-record-price-everything-to-know-now/

- Bureau of Economic Analysis – Official Q3 2025 GDP updated estimate showing 4.4% growth.https://www.bea.gov/news/2026/gross-domestic-product-3rd-quarter-2025-updated-estimate-gdp-industry-and-corporate

- CME Group FedWatch Tool – Real-time probabilities of Fed rate changes based on futures market data.https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

- ABC News – Coverage of stocks falling after Trump threatens European tariffs over Greenland.https://abcnews.go.com/Business/stocks-fall-trump-threatens-tariffs-european-countries-greenland/story?id=129377735

- Charles Schwab Market Update – Analysis of the “Sell America” trade and VIX spike on January 20.https://www.schwab.com/learn/story/market-volatility

- Bloomberg Markets – Live market coverage showing S&P 500 down 2.1%, volatility gauge at November highs.https://www.bloomberg.com/news/articles/2026-01-19/stock-market-today-dow-s-p-live-updates

- Yahoo Finance – Gold tops $5,000 in “breathtaking and profoundly scary” rally.https://finance.yahoo.com/news/gold-tops-5000-for-the-first-time-in-breathtaking-and-profoundly-scary-rally-013213150.html

- Charles Schwab Sector Outlook – Monthly analysis of S&P 500 sector ratings and performance.https://www.schwab.com/learn/story/stock-sector-outlook

- Barchart – U.S. GDP growth revised higher with corporate profits and inflation data.https://www.barchart.com/story/news/37186449/u-s-gdp-growth-revised-higher-in-q3-2025-as-corporate-profits-jump-and-inflation-holds-steady

- Trading Economics – Initial jobless claims data showing 200,000 for the week ending January 17.https://tradingeconomics.com/united-states/jobless-claims

- Morningstar – Analysis of Fed rate expectations for 2026.https://www.morningstar.com/markets/whats-next-fed-2026

- Federal Reserve Statement – Chair Powell’s statement on DOJ subpoenas and Fed independence.https://www.federalreserve.gov/newsevents/speech/powell20260111a.htm

- CNBC Powell Investigation – Coverage of DOJ criminal investigation into Fed Chair Powell.https://www.cnbc.com/2026/01/12/fed-jerome-powell-criminal-probe-nyt.html

- Ad Hoc News – AMD stock surge analysis as Intel struggles with supply constraints.https://www.ad-hoc-news.de/boerse/news/ueberblick/amd-s-stock-surge-fueled-by-rival-s-struggles/68517819

- Stocktwits Intel vs AMD – Comparison of chip stocks and Intel CFO comments on supply constraints.https://stocktwits.com/news-articles/markets/equity/intc-vs-amd-which-chip-stock-has-a-better-upside-this-year/cmybAivR4Xr

- FactSet Earnings Insight – S&P 500 earnings season update and sector-level expectations.https://insight.factset.com/sp-500-earnings-season-update-january-16-2025