TL;DR

A signed will feels like the finish line. It is not. One outdated form can hand a retirement account to an ex-spouse, a stranger, or the court. Six checks close the gaps. Each takes under a minute.

- The beneficiary form on your IRA, 401(k), and life insurance decides who inherits — your will never touches those accounts.

- Name your estate as beneficiary and the money drops into probate, opens to creditors, and can face a fast payout.

- A minor named directly triggers a court-appointed conservatorship, then a lump sum at the age of majority.

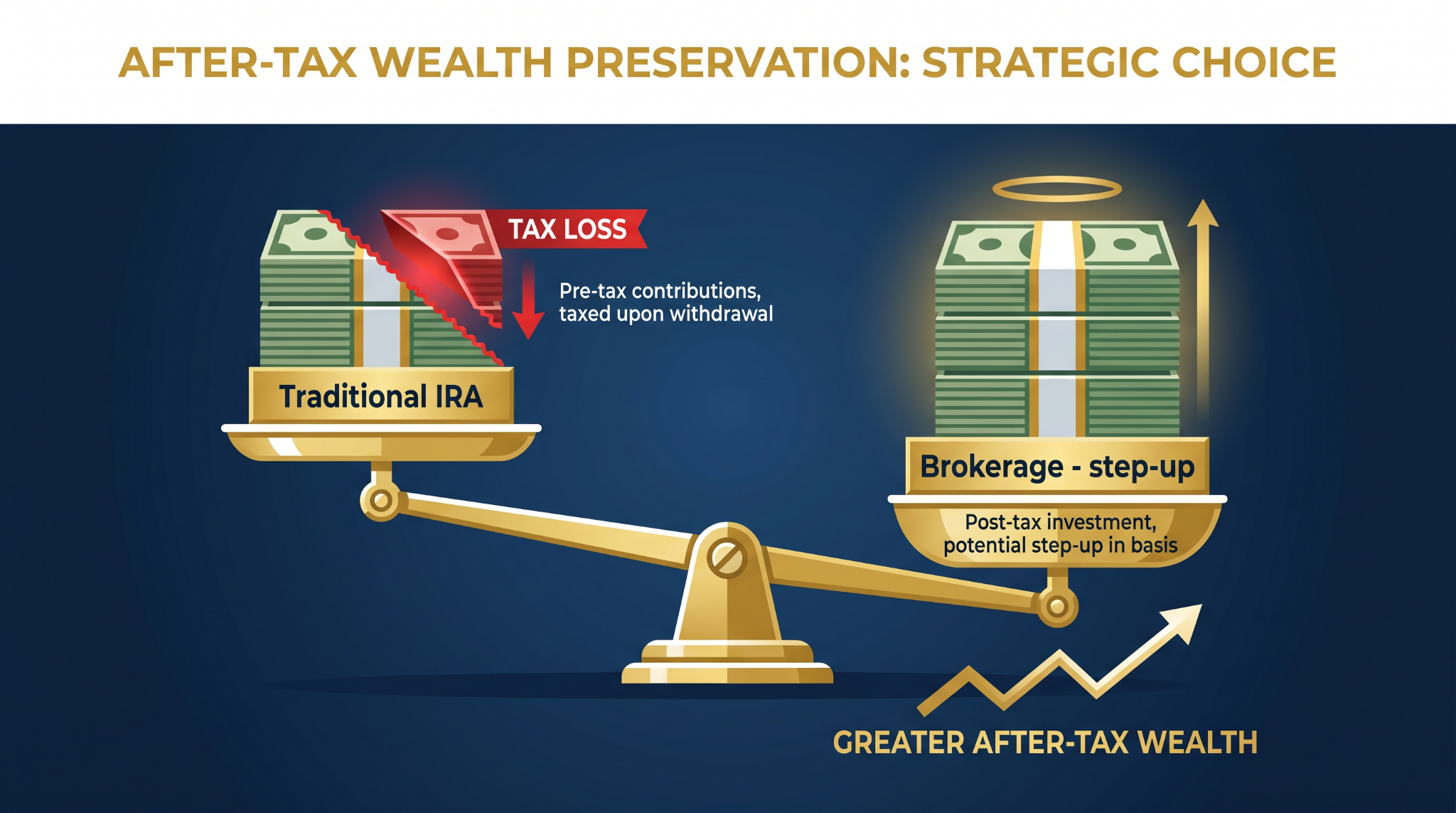

- Equal is not equal after tax: a traditional IRA is taxed as ordinary income, while a brokerage account gets a step-up in basis.

- A charity pays zero income tax on an inherited traditional IRA; your kids pay full freight on the same dollars.

- Most non-spouse heirs must empty an inherited account within ten years under the SECURE Act.

David L. Berkowitz, Investor and Financial Advisor

Nearly 40 years of experience — from trading and research at a $250 million hedge fund in the early 1990s, to two decades as a portfolio manager, to teaching thousands of executives and employees how to create shareholder value through EVA and value-based management. Now helping individuals and families become shareholders through disciplined investing, concentrated portfolios, and direct stock ownership.

Why your will loses to a form you forgot about

Most people spend hours on a will, sign it, and feel finished. Then one outdated form hands a retirement account to the wrong person. An ex-spouse. A sibling nobody has spoken to in years. Sometimes the court, not the family.

Beneficiary designations beat your will every time. The custodian pays whoever is named on the form. Your will never enters the room. The same goes for accounts titled joint with survivorship, Transfer on Death, or Payable on Death — they pass outside probate and skip the will entirely.

Here are the six checks. Grab a pen.

Check 1: The rule that beats your will

Which document actually controls your IRA? The beneficiary form. Not the will.

Your IRA, 401(k), life insurance, and annuities all pay the person named on the form. Courts will not override it to match your will. A couple came in last year for a plan review. The husband’s 401(k) still named his brother, from a form he signed in 1998, three years before he married his wife. Had he died, his wife would have received nothing from that account, and no judge could have fixed it. The form supersedes the will by law.

So pull up every account. Confirm the primary and contingent names match what you want today. Then check your titling — joint, TOD, and POD accounts pass by survivorship and bypass the will too. The gap here is silent. Nobody finds it until the money moves.

Check 2: The ‘my estate’ trap

Naming your estate as beneficiary sounds tidy. It does the opposite.

The moment your estate is the beneficiary, the account loses its protection and lands in probate. Probate is public, slow, and full of legal fees. It also opens the money to creditors. And because an estate is not a living person, the IRA can be forced empty on a compressed schedule instead of stretching over years. One client had named her estate as the contingent on a $600,000 IRA. She thought it was a safe default. We switched it to named people and kept that account out of court entirely.

Two fixes. Strip the words ‘my estate’ from every primary and contingent line. Then name a contingent on every account, so nothing falls back to the estate if your first choice dies before you.

Check 3: Keep minors off the form

Can you leave a large account straight to a grandchild? No. The custodian will not release it to a minor.

Name a child directly and a court steps in. A judge appoints someone to manage the money through a conservatorship, on your family’s dime, until the child reaches the age of majority. Then the child receives the full amount in one shot — at an age most of us were not ready to handle it. Many custodial accounts hand over the entire balance at 18 or 21.

Route the money through a structure instead. A trust, living or testamentary, or a UTMA account with an adult custodian. That controls when the money is released and who watches it. If you have minor beneficiaries anywhere, this is worth a call to your attorney this week.

Check 4: Equal is not equal

This is the check that splits families. Same face value, very different after-tax checks.

Say you leave your son a $200,000 traditional IRA and your daughter a $200,000 brokerage account. On paper, fair. In reality, your son owes ordinary income tax on every dollar he pulls from that IRA. Your daughter inherits her account with a step-up in basis — the built-in gains are wiped clean at death.

The numbers make the gap obvious:

| Heir | Account inherited | Face value | What the tax code does |

| Son | Traditional IRA | $200,000 | Ordinary income tax on every dollar withdrawn. At a 24% rate, roughly $48,000 goes to the IRS. |

| Daughter | Taxable brokerage | $200,000 | Step-up in basis wipes out the built-in gain at death. She can sell near $200,000 with little or no tax. |

Illustrative only; actual tax depends on each heir’s bracket. So inventory your accounts by tax type. Pre-tax IRAs and 401(k)s on one side. Roth accounts, taxable brokerage, and cash on the other. Then adjust the designations so heirs land at equal after-tax amounts, not equal sticker prices.

Check 5: Give the taxable accounts away

This one matters only if you give to charity. It saves real money.

A charity pays no income tax on an inherited traditional IRA. Your kids pay full income tax on the same dollars. So point your most tax-heavy assets at the charity — traditional IRAs, non-qualified annuities, the accounts that hand your heirs a tax bill. Send those to the causes you support, and the tax disappears.

Then save the good stuff for family. Roth IRAs and appreciated stock that gets the step-up. Same total gift, thousands of dollars less lost to taxes.

Check 6: Trusts, multiple heirs, and the SECURE Act

This is where people trip on the fine print. Three traps.

First, trusts. Name a trust as the beneficiary of an IRA and it has to qualify as a see-through trust. Get the language wrong and the account can be forced empty on a five-year clock — a tax squeeze your heirs feel right away. Confirm the wording with your attorney.

Second, multiple heirs on one IRA. The designated beneficiary is locked in by September 30 of the year after death, and heirs left sharing a single account can be pushed onto the oldest one’s timeline. The fix is a deadline: split the money into separate inherited IRAs by December 31 of that same year, so each heir uses their own life expectancy. Under the SECURE Act ten-year rule, most non-spouse heirs still have to empty the account within ten years — but eligible designated beneficiaries, like a surviving spouse or a disabled heir, are exempt.

Third, annuities. Name a trust on a non-qualified annuity and you can trigger immediate taxation, stripping the tax deferral you paid for. Check that one carefully before you sign.

Run the whole check in one pass

Here is the full sequence. Confirm every name matches your wishes today. Strip ‘my estate’ off the forms and add contingents. Keep minors out of direct designations. Balance heirs by after-tax value. Send tax-heavy accounts to charity. Get the trust and multi-heir rules right.

| # | Confirm this | The fix |

| 1 | Every primary and contingent name matches what you want today. | Pull each account. Update stale names. Check joint, TOD, and POD titling too. |

| 2 | No account names ‘my estate’ on any line. | Remove ‘my estate.’ Name real people. Add a contingent to every account. |

| 3 | No minor is named directly. | Route the money through a trust or a UTMA account with an adult custodian. |

| 4 | Heirs are balanced by after-tax value, not sticker price. | Sort accounts by tax type. Adjust shares so heirs land at equal after-tax dollars. |

| 5 | Tax-heavy accounts point to charity if you give. | Send traditional IRAs and annuities to charity. Leave Roth and appreciated stock to family. |

| 6 | Trust and multi-heir language is correct. | Confirm see-through trust wording. Split multi-heir IRAs into separate inherited accounts. |

Do it once a year, and after any big life event — a marriage, a divorce, a birth, a death, or a change in the tax law. Designations only work if you keep them current. When you finish, request updated beneficiary forms from each custodian and send a copy to your advisor, so your plan and your accounts actually agree.

This walkthrough is educational, not legal or tax advice. Beneficiary rules turn on your state and your exact accounts, so confirm the trust and annuity language with a qualified attorney or tax professional who knows your full situation before you sign.

Endnotes

1. The beneficiary form controls who inherits — Edelman Financial Engines explains why beneficiary designations override the instructions in a will. https://www.edelmanfinancialengines.com/education/estate/beneficiary-designation-vs-will/

2. designations supersede the will by law — Trust & Will on keeping designations current because they control regardless of the will. https://trustandwill.com/learn/beneficiary-designation-vs-will

3. TOD, POD, and joint accounts pass outside probate — ElderLawAnswers on how payable-on-death and transfer-on-death accounts transfer by operation of law and bypass probate. https://www.elderlawanswers.com/passing-on-assets-outside-of-probate-pods-and-tods-15137

4. naming your estate drops the account into probate — Kiplinger on why naming your estate as IRA beneficiary forces probate, exposes the money to creditors, and can accelerate the payout. https://www.kiplinger.com/retirement/retirement-plans/iras/604980/dont-name-your-estate-as-your-ira-beneficiary

5. A minor triggers a court-appointed conservatorship — Policygenius on how a UTMA custodian manages a minor’s money until the age of majority, and what happens without one. https://www.policygenius.com/estate-planning/utma-account/

6. custodial accounts release the full balance at majority — Chase on custodial accounts transferring the entire balance to the child at the age of majority. https://www.chase.com/personal/investments/learning-and-insights/article/custodial-accounts-when-child-turns-18

7. step-up in basis wipes out built-in gains at death — Fidelity explains how inherited taxable assets get a cost basis reset to date-of-death value. https://www.fidelity.com/learning-center/personal-finance/what-is-step-up-in-basis

8. Inherited traditional IRAs get no step-up — LegalClarity on why inherited IRAs are income in respect of a decedent, get no step-up, and are taxed as ordinary income. https://legalclarity.org/do-inherited-iras-get-a-step-up-in-basis/

9. A charity pays no income tax on an inherited IRA — Fidelity Charitable on how a tax-exempt charity avoids income tax on inherited retirement assets that would tax heirs. https://www.fidelitycharitable.org/guidance/philanthropy/donating-retirement-assets-to-charity.html

10. A trust must qualify as a see-through trust — Fidelity on the see-through trust requirements for a trust named as an IRA beneficiary. https://www.fidelity.com/viewpoints/wealth-management/insights/iras-left-to-a-trust

11. The SECURE Act ten-year rule — IRS Retirement Topics — Beneficiary: most designated beneficiaries must empty the account by the end of the 10th year after death. https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-beneficiary

12. The designated beneficiary is determined by September 30 — IRS Publication 590-B on determining the designated beneficiary and the separate-account rules for inherited IRAs. https://www.irs.gov/publications/p590b

13. Eligible designated beneficiaries are exempt — Charles Schwab on the eligible-designated-beneficiary categories that are exempt from the ten-year rule. https://www.schwab.com/learn/story/inherited-ira-rules-secure-act-20-changes

14. A trust on an annuity can trigger immediate taxation — My Annuity Store on how naming a trust on a non-qualified annuity can end tax deferral and accelerate taxation. https://myannuitystore.com/retirement-planning/transferring-annuity-to-trust/